Bill Ackman likes to hunt for big, mispriced assets...

Bill Ackman likes to hunt for big, mispriced assets...

The Pershing Square CEO famously turned a $27 million bet in early 2020 into a $2.6 billion payout when the market crashed.

His latest target is Universal Music Group (UMG.AS). And he's going after it with a €55 billion deal. The Universal listing would also move from Amsterdam to New York (the New York Stock Exchange).

That's a huge development for the world's largest record label. And the market noticed it right away...

UMG shares jumped 11.4%, from €17.10 to €19.06, after Pershing Square laid out its terms on April 7. The surge came after the stock fell more than 30% over the previous six months.

Ackman is willing to pay a hefty price for Universal. But can a new U.S. listing unlock the true value of one of the world's deepest music catalogs?

There's as much value in the listing as in the songs...

Universal sits at the center of the global music business. The company is home to artists like Taylor Swift and Kendrick Lamar. It raked in €12.5 billion in revenue last year alone.

Ackman believes that owning elite music rights could generate big royalty streams for decades. Unlike most businesses, a strong music catalog doesn't depreciate… A Beatles song, for example, generates just as much in royalties today as it did 20 years ago.

He also believes that the market has been mispricing those assets... It's treating Universal like a sleepy European listing instead of a rare asset with long-term earning power.

Ackman's solution is to put the company in front of a deeper investor base.

The U.S. market tends to reward businesses with strong intellectual property...

Universal already has an impressive music catalog. And it has a recurring royalty engine that investors usually pay a premium for.

Pershing Square's €55 billion deal reflects Ackman's confidence. There could be a lot of value trapped inside the current Universal setup.

According to Ackman, the deal implies a value of €30.40 per share. That's far above the level it reached even after the recent rally.

The price ultimately depends on two factors – a higher valuation for the new U.S.-listed company, and the sale of Universal's stake in Spotify (SPOT) for €1.5 billion in net proceeds.

Under the current proposal, Universal shareholders would receive €5.05 in cash, or about €9.4 billion in total. They would also get 0.77 shares in the new company (post-merger) for every share they own today.

Ackman didn't dream this up overnight. Pershing built roughly a 10% stake in Universal in 2021, ahead of its Amsterdam listing.

Ackman also joined the board and became one of the company's loudest supporters. He argued that music rights from artists like the Beatles to Taylor Swift can generate "forever" cash flows.

The same message applies today. Universal owns rare assets, and the market still undervalues them...

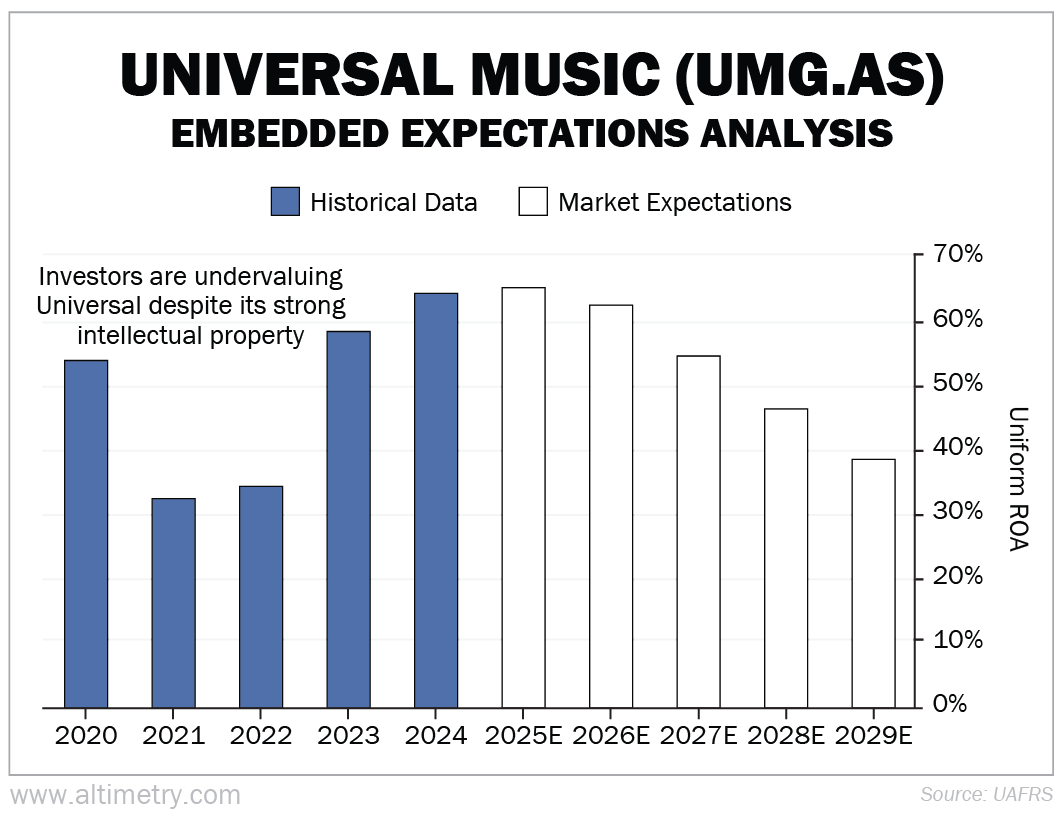

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Universal's Uniform return on assets ("ROA") has risen above 32% every year for the past five years. It has gotten as high as 64%.

Despite this, investors only expect a Uniform ROA of 39% in the future. Take a look...

Simply put, the market is valuing Universal like a sluggish European media stock. But its strong music catalog and a potential U.S. relisting are likely to boost profitability.

We don't know if Ackman's deal will actually cross the finish line...

But investors don't need every part of the Pershing Square-Universal merger to succeed to profit from his thesis...

At roughly €19 per share, Universal still trades far below Ackman's €30.40 implied value.

That means the market is still weighing a few factors. These include AI-related copyright fears and the current Amsterdam listing, which hasn't attracted the right audience.

Also, any transaction would need major support from Universal shareholders.

The company may have more upside via steady growth and greater investor recognition. After all, Universal's catalog is one of the rarest assets in all of media.

Whether or not Ackman's deal goes through, Universal is a stock worth keeping a close eye on.

Regards,

Joel Litman

April 22, 2026