Netflix (NFLX) made the wrong kind of history last week...

Netflix (NFLX) made the wrong kind of history last week...

For the first time in a decade, streaming king Netflix lost more than 200,000 subscribers in the first quarter. The first down quarter in a decade sent the stock plunging more than 35% on Wednesday, and it has continued to fall since.

Netflix was once thought to be an untouchable member of the FAANG stocks – alongside Meta Platforms (FB), Apple (AAPL), Amazon (AMZN), and Alphabet (GOOGL). Over the past decade, these Big Tech names have historically carried huge gains in the S&P 500. Now, investors are scratching their heads as to how such a mighty name has fallen.

Reed Hastings, CEO of Netflix, cites increasingly fierce competition from other streaming players like Disney's (DIS) Hulu and Disney+, along with a subscriber loss of Russian accounts being closed following the country's invasion of Ukraine. Hastings also warned that the loss is just beginning, and losses could be as high as two million next quarter.

While the market was shocked, there had been writing on the wall...

Back in 2020, we recognized Netflix's power to continue disrupting the traditional theater and content markets as the coronavirus pandemic reared its ugly head. That is why in May 2020, we recommended Altimetry Hidden Alpha readers buy Netflix stock.

However, a year later, the story began to change. We sent out the following message to tell our readers that investors were expecting too much from Netflix:

While Netflix still has an impressive brand and is a great business, it's moving from a position of strength to a position of parity. As management spends more and more of its capital creating content instead of being a content aggregator, it has to compete with companies like Disney at their own game.

We still like Netflix, but we have to look at the name in a vacuum as opposed to an investment already in the portfolio – which is how any portfolio analyst worth his salt assesses a name. We wouldn't be recommending a market leader with a target on its back and continued high expectations for growth.

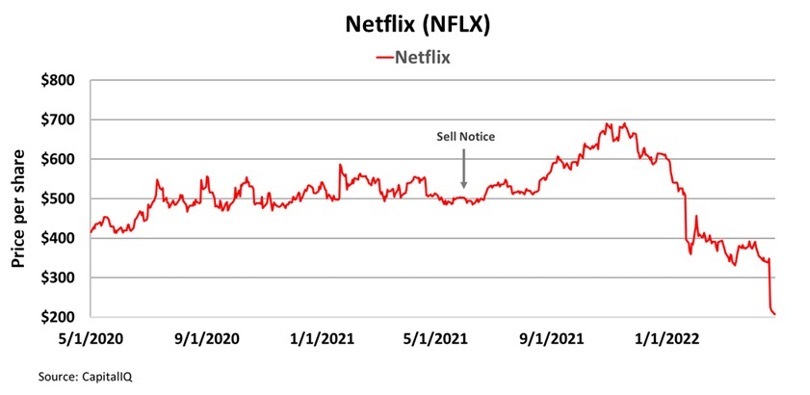

In the chart below, you can see the path of Netflix's stock and where we told our readers to get out. Readers that followed our advice made a respectable 19% gain rather than experiencing a staggering 50% loss if they had held on through today.

With Netflix down so much, some readers may be wondering if they should buy back into the FAANG stock at a discount.

To understand whether Netflix could be a buy, we need to understand what the market is pricing in at current valuations, and we need to put those expectations into the context of the company's position in the competitive streaming landscape.

For getting a handle on valuations, we can turn to our Embedded Expectations Analysis ("EEA"), which breaks down market expectations for future returns.

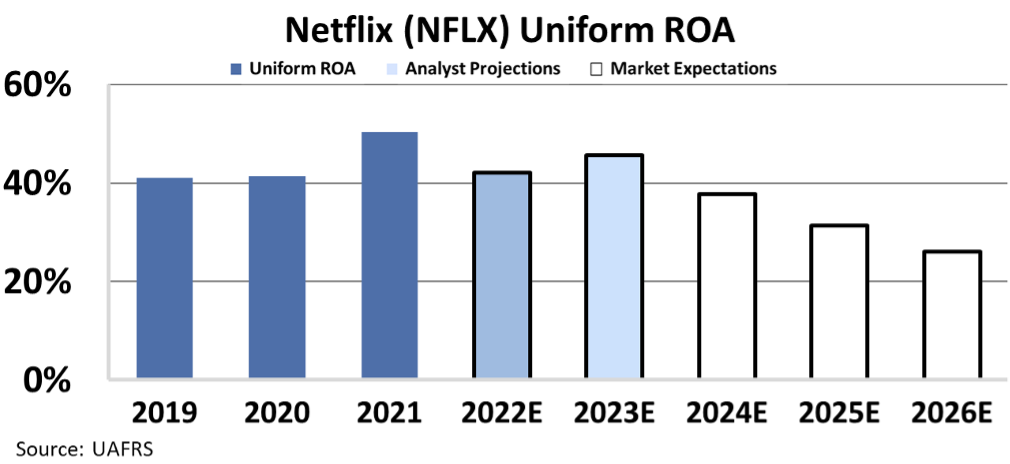

In the chart below, we can see how at recent lows, the market expects Uniform return on assets ("ROA") to fall to 20%, a huge reversal from the 2021 pandemic highs, when folks were subscribing to services like Netflix in droves.

Looking at the EEA chart, it may seem like if Netflix cleared 20% returns over the next few years, the stock could jump back up.

However, if a company is cheap, that alone doesn't mean you should buy it. This is why we don't recommend every name that looks cheap through the lens of Uniform Accounting... And sometimes we even recommend names that look expensive.

To figure out if a name is cheap for a reason, or rightfully valued at a premium, we have to look deeper at the company's fundamentals. Going back to our Netflix sell notice, we highlighted how growth is the business' Achilles' heel, not returns.

For Netflix, growth, which is best represented by subscriber growth, signaled collapse for the stock. Netflix's investor base is predominantly growth funds, who are now going to be active sellers, putting long-term pressure on the stock.

Until there's a changing of the guard and Netflix can either break the cycle of slowing growth or begin to see an influx of value-focused investors who won't be worried about slower growth, the stock price won't rise.

Netflix is a valuable lesson to not just focus on valuations, but to also look at the fundamentals. Even with the stock trading for cheaper than ever, it's still a name to avoid.

Regards,

Joel Litman

April 27, 2022