JetBlue Airways (JBLU) built a reputation on making flying a little less miserable...

JetBlue Airways (JBLU) built a reputation on making flying a little less miserable...

The airline offered free Wi-Fi, plus more legroom and friendlier customer service than other budget carriers. It created a decent image in an otherwise brutal business.

That perception has changed, though... and fast.

For one, JetBlue has been struggling with delays... It ranked among the worst airlines in that category in 2023. It's also charging passengers to check their luggage and forcing travel companions to pay a premium just to sit together.

But JetBlue is trying to turn things around. The company is considering a potential sale and consolidation with United Airlines (UAL), Alaska Air (ALK), or Southwest Airlines (LUV).

This comes after a U.S. federal judge blocked JetBlue's acquisition of Spirit Airlines in 2024. (He said it violated antitrust laws.)

JetBlue's shares have fallen more than 30% since the start of 2025. And now it's looking for a life raft.

Before any deals go through and investors think about piling in, they need to understand the difference between a cheap stock and a cheap business.

The airline's recent collapse seems like a tempting buying opportunity...

A stock that drops 30% will always attract bargain hunters... especially where networks and scale can create real value.

You see, the airline industry relies on "network effects." The value of an airline's network increases with each new city or route it adds. A strong, growing network reduces costs, improves passenger flow, and boosts profitability.

But JetBlue isn't expanding its network. The company has struggled to regain its footing since the COVID-19 pandemic. And it's losing ground at both ends of the market...

JetBlue can't keep up with premium-focused carriers like United and Delta Air Lines (DAL). Also, discount travelers are gravitating toward Spirit and Frontier.

That leaves JetBlue stuck in the middle. That's not where you want to be.

JetBlue may not be profitable enough to attract a key industry player...

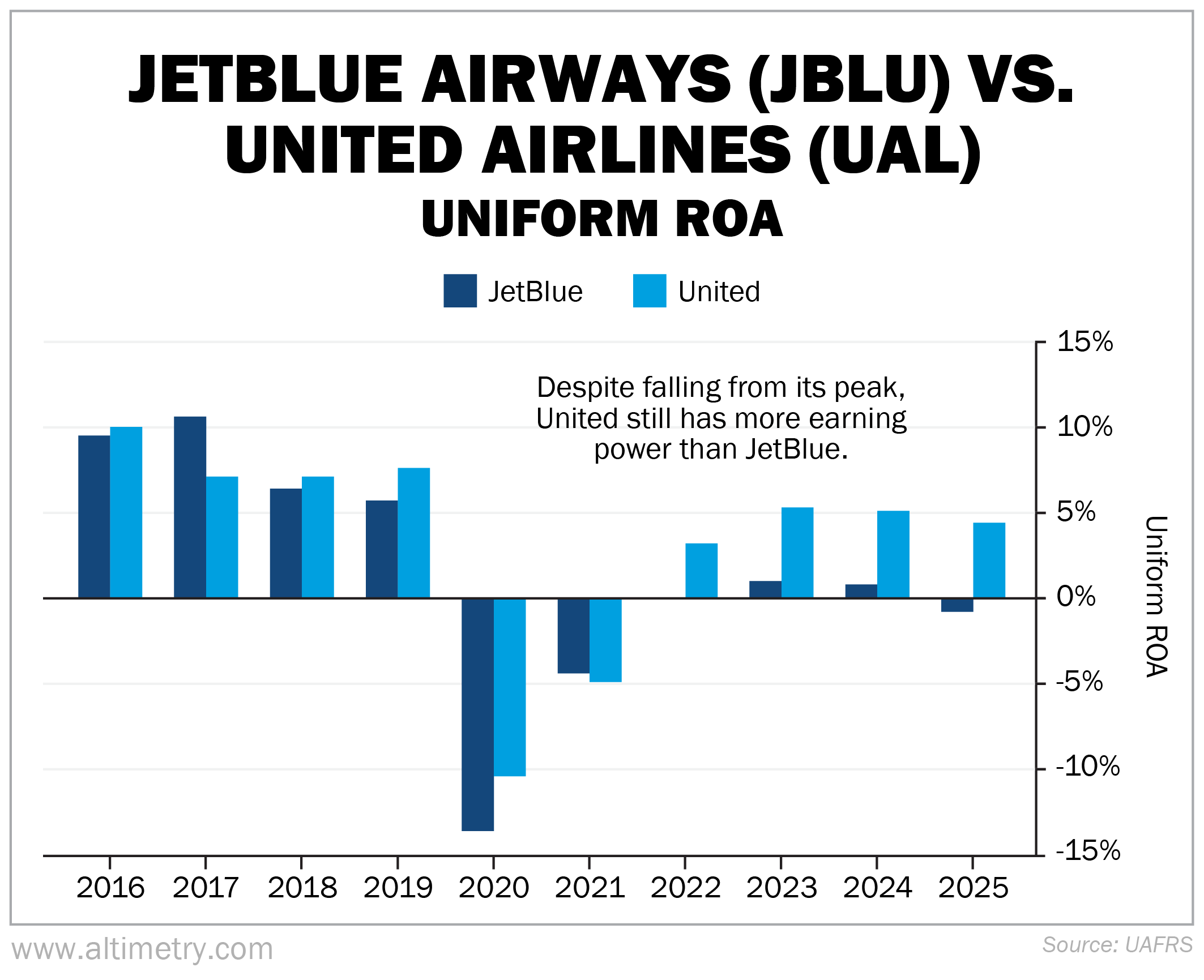

In its heyday, JetBlue's Uniform return on assets ("ROA") peaked at 11% – just under the 12% corporate average. That was in 2017.

Then, the business started to soften. Returns began slipping in 2018, before the pandemic exposed a more serious weakness. JetBlue's Uniform ROA fell to negative 14% in 2020, and it has hovered around zero ever since.

Airline consolidation only works when the target company is worth integrating. If the buyer spends years fixing routes, adjusting costs, and smoothing out customer relationships, the merger becomes more of a repair job than a value-add.

United has had its own issues, too, including scrutiny over aircraft safety and maintenance. But it's in a much healthier financial position than JetBlue.

Before the pandemic, United's average Uniform ROA was about 8%. Over the past four years, that figure has fallen closer to 4%. Take a look at the companies side by side...

It's also worth noting that JetBlue and United launched a partnership in late 2025 called "Blue Sky." It allows customers to earn and redeem points and miles on flights operated by either carrier.

This has strengthened JetBlue's network, but it still needs help.

And United may be in a good position to rescue JetBlue. But that doesn't mean the business is worth salvaging.

United can put its money to better use...

JetBlue has trailed far behind United and Delta over the past few years.

News of a potential takeover did spark a one-day jump. But JetBlue's stock has remained in negative territory since early 2025.

As a result, United is cautious about the purchase price it would accept in a JetBlue merger.

Right now, United is focused on bumping up its credit rating from "high-end speculative" to "investment grade"... Its strong cash flow and lower debt are paving the way.

Absorbing a heavily indebted JetBlue would make that harder. A full merger – beyond the Blue Sky partnership – would strain United's finances and invite antitrust scrutiny.

That's a lot to take on for a company that still has room to improve. The bottom line is, United doesn't need to buy a fixer-upper to create value for its shareholders.

Regards,

Joel Litman

April 16, 2026