Two conflicting trends are now converging...

Two conflicting trends are now converging...

And it might be the best possible outcome for the rest of the economy.

Regular readers know we've pointed out a dramatic surge in mergers and acquisitions (M&A). This year is shaping up to be one of the most active for deals since 2021.

As we wrote earlier this month, it's a clear sign that credit conditions are improving... corporate confidence is rising... and businesses are ready to build again.

On what seems like an unrelated note, we've written previously about an ongoing long freeze in private equity ("PE"). PE has been all but dormant for nearly two years. Many firms have been unable to dump companies they no longer want to hold.

A lot of PE-backed companies end up going public... usually. But several high-profile initial public offering ("IPO") flops in 2023 slowed the PE IPO market.

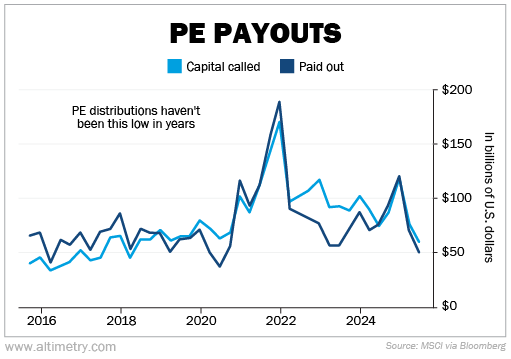

Industry-wide distributions (or the money distributed to investors) fell to their lowest levels since the depths of the pandemic. PE firms are now under pressure to sell their companies no matter the price.

And that pressure is starting to thaw out this once-frozen market.

Folks, these two trends – the M&A surge and the PE thaw – seem distinct at first glance.

But they're now converging. And it's telling us a lot about today's economy...

PE is finally accepting lower prices just to get deals done...

These firms haven't had a lot of chances to sell since 2021.

High interest rates made it far more difficult for the industry to operate. PE firms usually buy companies with debt to increase their returns.

And with interest rates as high as 4.5% this year, those deals got a lot less lucrative.

Higher debt made it harder for PE to justify new acquisitions... and harder to find buyers for the ones they already held.

It has been a long standoff. But now, that standoff is ending.

Blackstone (BX), one of the industry's largest players, is on track to sell more than $30 billion worth of companies in its portfolio... more than any time since the 2021 boom.

Blackstone President Jon Gray said last month that "the deal dam is breaking."

Others haven't been as fortunate. Carlyle (CG) just reported its weakest exit quarter since 2020, with only $2.3 billion in realized proceeds.

Investor patience has run dry...

In the second quarter of 2025, industry-wide distributions totaled less than $52 billion... the lowest level since the abysmal first and second quarters of 2020.

Check it out...

PE firms should be panicking. If their investors aren't happy, they have no way of raising money for new investments.

Carlyle seems to understand this. It knows its investors want to cash in on their investments. So it's promising brighter days in the near future... lining up $5 billion more in expected sales to close the year.

With IPOs still hit-or-miss, other PE firms are turning to strategic buyers – companies in the same industry that want to fold a smaller business into existing operations.

Right now, strategic buyers have all the leverage. Many PE firms are forced to accept fire-sale prices.

But while this setup is painful for fund managers, it's a boon for the companies doing the buying...

And it's great for the economy at large.

The M&A wave of 2025 has already put us on track for the biggest or second-biggest deal year in history.

All those cheap PE deals are helping boost overall M&A volume even further. And they're making it easier for those deals to create value by enhancing earnings.

We've said it before, but it bears repeating... Record-level dealmaking doesn't happen in a weak economy.

Neither does a fire-sale exit wave from an industry as large and interconnected as private equity.

Price typically determines the success of acquisitions...

The more expensive the deal, the less likely it will be worth it... at least, not without some serious legwork from the acquirer.

In other words, cheap deals are good for pretty much everybody outside of the PE industry.

That's not just a win for shareholders. It's a tailwind for the broader economy. All these PE deals will help drive earnings (and the market) higher.

Regards,

Joel Litman

November 21, 2025