AI spending is getting bigger than most companies can afford...

AI spending is getting bigger than most companies can afford...

Google parent Alphabet (GOOGL) already expects to spend as much as $190 billion on capital expenditures this year.

Much of that cash is going into the physical backbone of AI... data centers, chips, power, and the custom infrastructure needed to keep up with the AI boom. Next year, Bloomberg Intelligence estimates the number could reach $300 billion.

At that level, Alphabet would be investing more in growth than it generates in operating cash flow.

That is a strange place to be for one of the world's largest companies. Alphabet has spent years throwing off enough cash to do whatever it wanted.

In fact, it couldn't put all that money to work on projects fast enough. The Big Tech giant has spent almost $350 billion buying back its own stock in the past decade.

But AI has changed the equation. Earlier this month, Alphabet spooked investors when it announced a huge equity raise. But as you'll see, it's not a sign of weakness in the business.

Far from it...

The deal sounds massive at first glance... and that's what is scaring the market...

Alphabet is working on an $80 billion equity raise to help fund its AI-infrastructure expansion.

The plan has several pieces. Alphabet expects to raise $40 billion through an at-the-market program... which lets it sell some of the shares it owns into the market.

Warren Buffett's former holding company, Berkshire Hathaway (BRK-B), is investing another $10 billion directly.

The remaining $30 billion comes from new offerings of common stock and mandatory convertible preferred shares. (Preferred shares trade like common equity and receive a special dividend for a set period, then convert into regular shares.)

Investors are always touchy about equity raises once a company is already public. New stock can "dilute" current shareholders. It can also signal that management thinks the stock is expensive... and it's time for folks to cash in while they can.

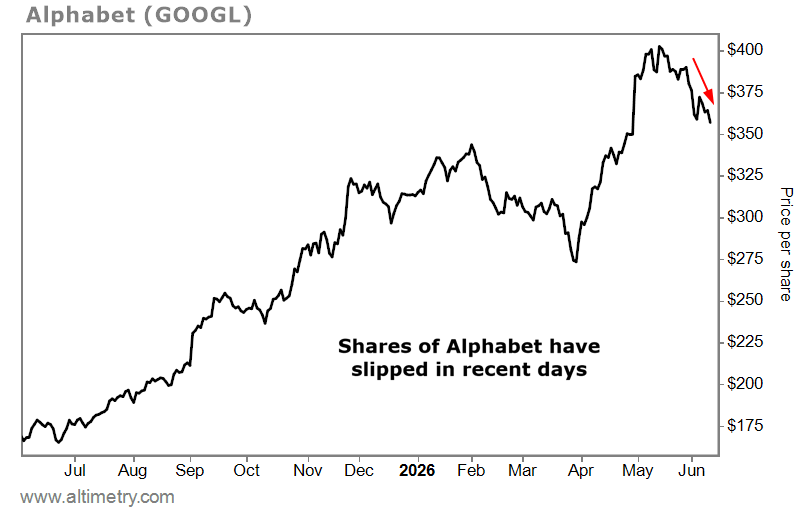

Alphabet's stock has more than doubled over the past year. But shares still fell after the announcement. Take a look...

We're talking about the second-largest company in the world behind AI darling Nvidia (NVDA). Alphabet's market cap is more than $4 trillion as we go to press. An $80 billion raise is less than 2% of that.

That's a tiny price to pay to let the company fund another year of AI investment capacity. But shareholders seem to think otherwise.

Companies do sometimes cash in when their stocks are overvalued...

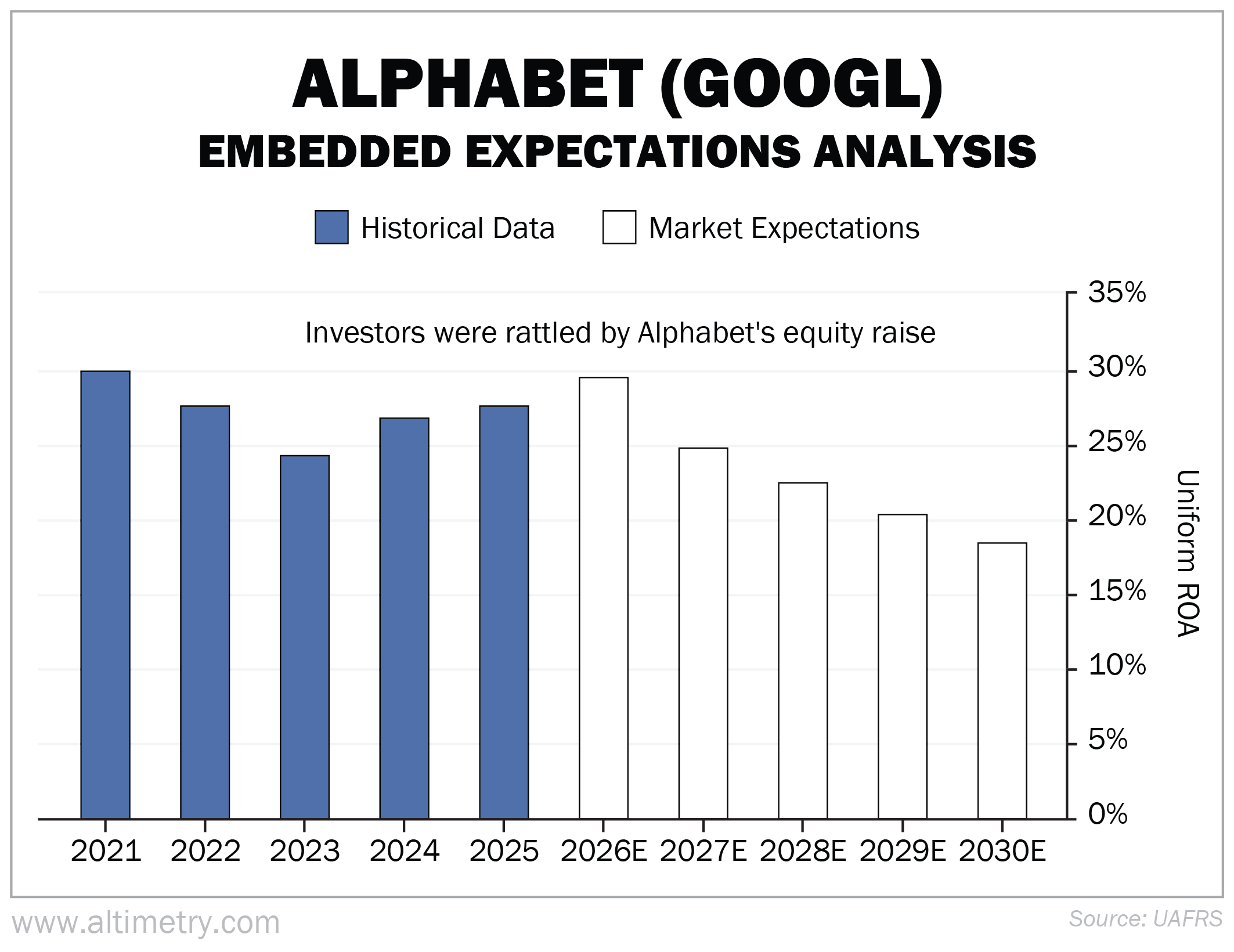

But that doesn't seem to be the case here. We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Alphabet's Uniform return on assets ("ROA") has been above 20% for its entire history. It has stayed above 24% since 2021.

And yet, after the stock's recent dip, investors are acting as if Uniform ROA will fall to just 18%.

Check it out...

Investors are treating the AI build-out as a drag on profitability. But Alphabet's track record speaks for itself.

It has already proved it can turn huge infrastructure investments into a dominant force in AI.

Alphabet has already raised more than $80 billion in debt over the past year...

It also generated about $174 billion in operating cash flow over the 12 months ended in March. Now, this equity raise adds another massive funding source.

All of these factors help the company stay on track with its spending expectations. This equity raise is a tiny expense in the grand scheme of things.

Investors should be treating it as an investment in keeping Alphabet at the head of the AI race. Instead, they're punishing Alphabet for doing more of what has worked for years.

It's hard to imagine that one of the biggest companies on Earth could be cheap. Based on what we're seeing, though... Alphabet may be exactly that.

Regards,

Joel Litman

June 11, 2026