Entertainment titan Disney (DIS) may be reaching a breaking point...

Entertainment titan Disney (DIS) may be reaching a breaking point...

For years, the company has suffered many setbacks... In 2020 and 2021, the pandemic emptied Disney's theme parks and shuttered movie theaters where Disney's films typically debuted. In 2022, a troubled leadership transition brought Bob Iger back as CEO and added years of strategic uncertainty. Then Disney poured billions of dollars into its streaming platform, Disney+, just as its legacy businesses were trying to recover.

All of this has taken a toll on the stock. In the past five years, Disney shares have lost nearly half their value, while the S&P 500 Index has climbed more than 70%.

Now, financial-services company Wells Fargo is pushing a dramatic solution to Disney's problems... It says Disney should abandon Disney+, license its deep content library to other streaming platforms, and refocus on intellectual property and experiences. Wells Fargo estimates that the shift could raise the stock's price by roughly 40%.

Today, we'll examine whether walking away from streaming would repair Disney's business model... and give investors a reason to expect a share-price recovery.

Disney+ launched at the worst possible moment...

On November 12, 2019, the streaming platform was released in the U.S. and Canada. Then on March 24, 2020, it expanded to Western Europe. Around that same time, the world was going into lockdown because of COVID-19. You might think that billions of folks stuck at home would give Disney+ an instant win.

However, a global streaming service requires a large technology platform, and it takes a lot of money to grow a customer base. That meant Disney had to spend heavily to win subscribers. It was shelling out hundreds of millions of dollars on advertising and offering discounted subscriptions to attract new customers – all while funding a steady flow of exclusive programming.

Those costs hit just as the rest of the company was under severe pressure from the pandemic.

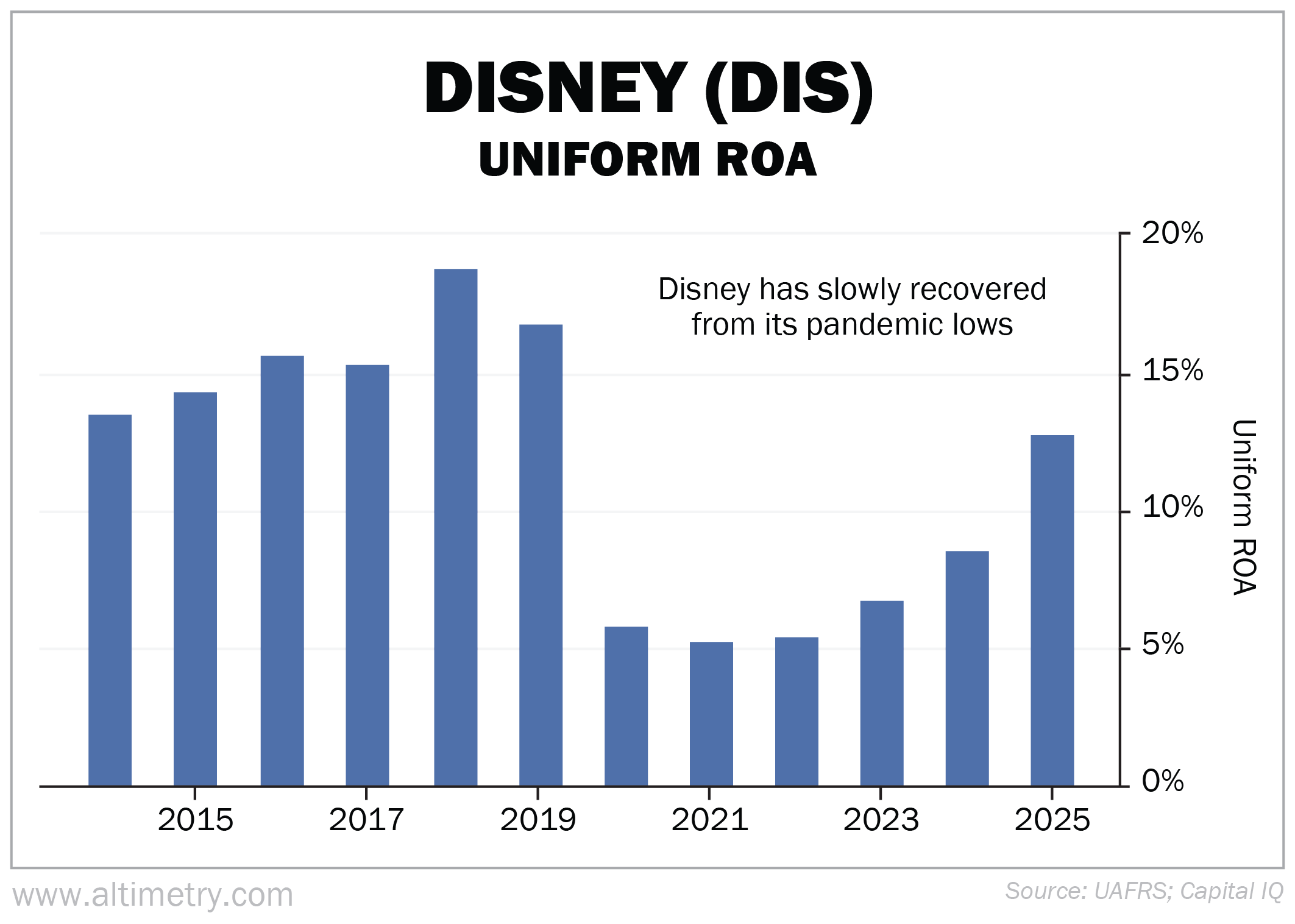

Disney's Uniform return on assets ("ROA") reached an all-time high of 19% in 2018. By 2020, the pandemic and the streaming ramp-up had driven Uniform ROA down to 6%.

Since then, Disney has at least stopped the bleeding... Its Uniform ROA climbed back to 13% last year, showing that the worst of the Disney+ investments are in the past. Take a look...

Despite this improvement, Disney is far less profitable than it was before it built Disney+. That's why Wells Fargo is pushing for it to scrap the streaming service and license its content to competitors.

See, Disney's advantage lies in the content itself...

Its animated classics, Pixar films, Marvel stories, and Star Wars universe can travel across platforms and markets for decades. Rival streamers need quality programming to convince folks to subscribe to their service... And Disney controls some of the most valuable, beloved franchises in entertainment.

Wells Fargo estimates that a content-first model could produce more than $15 billion in annual licensing revenue. Unlike operating a streaming platform, Disney licensing its content would require far less investment in technology and marketing, allowing more of that revenue to flow to the company's bottom line.

In other words, Disney could let other companies handle the expensive business of streaming while it focuses on creating the content audiences actually want to watch – and while collecting premium fees for its existing content.

Whether management follows Wells Fargo's strategy or not, Disney is under increasing pressure to do something to improve its economics. Because right now, investors don't have a great long-term outlook...

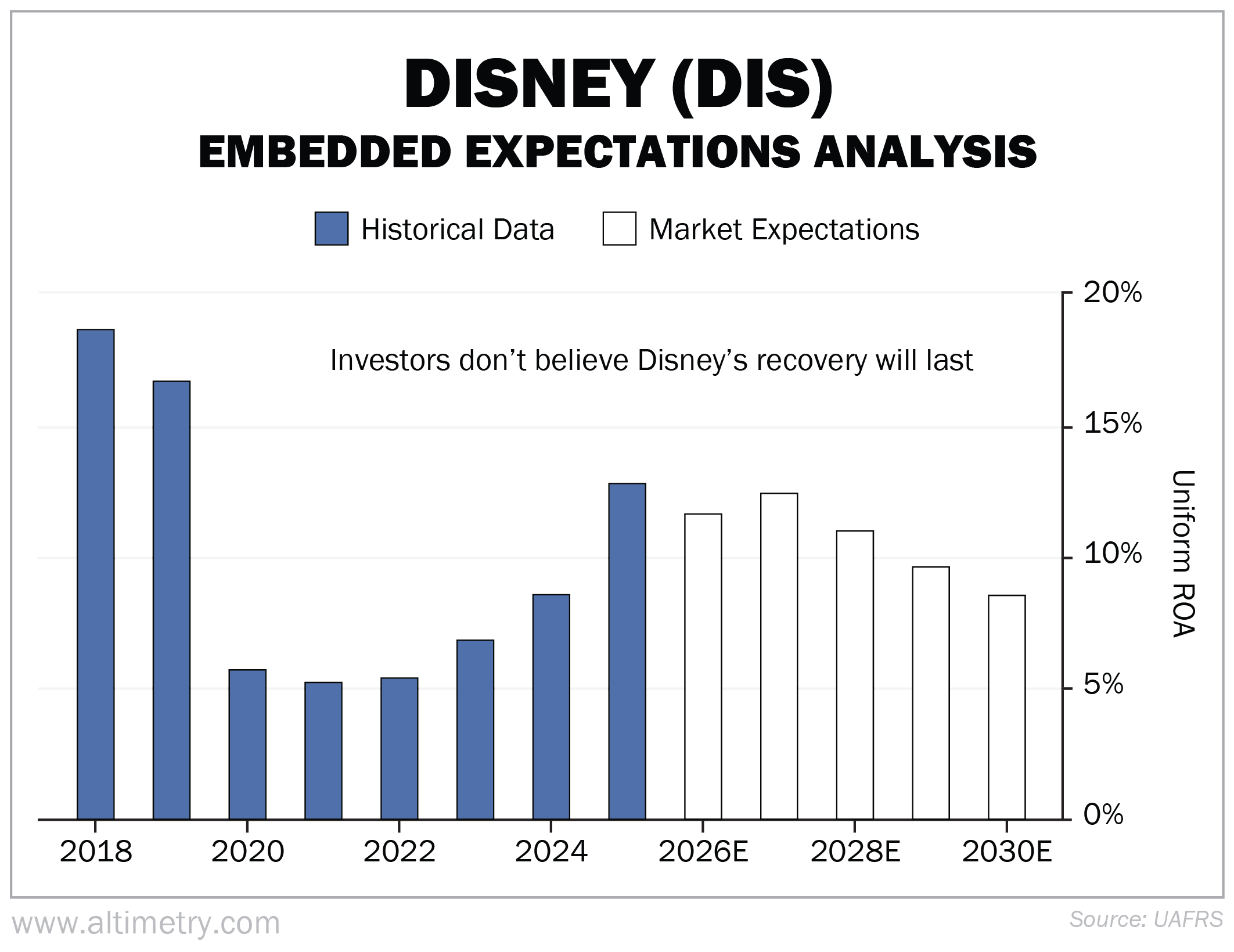

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

As you can see below, the EEA shows that investors expect Disney's Uniform ROA to fall to roughly 9% by 2030, well below last year's 13%. This tells us the market believes Disney's recent recovery will stall and that profitability will fade again...

However, if Disney licenses its content, it could return to pre-2019 profitability...

As we covered earlier, Disney's ROA hit an all-time high in 2018, the year before it launched Disney+. Since then, the company has been struggling.

Wells Fargo has offered a solution to Disney's profitability problems. Now, it's just a matter of whether management is willing to scrap the streaming service.

There's a good chance the team won't want to throw out the billions of dollars it has poured into developing Disney+. So until management commits to a clear plan to improve profitability, there's no reason for investors to get excited about this stock or expect shares to return to previous highs.

We recommend you keep away from Disney for now.

Regards,

Joel Litman

July 14, 2026