NATO is prepping for a historic spending spree...

NATO is prepping for a historic spending spree...

The U.S. contributes 16% of NATO's total defense budget. But rising tensions with Russia – along with political pressure from the Trump administration – are forcing European allies to step up.

Member states are preparing to commit a staggering 5% of their GDP to defense-related investments by 2032. This marks a full-scale rearmament not seen since the Cold War.

And a Bloomberg report reveals that negotiations are already underway.

The new target combines 3.5% in direct defense spending, with an additional 1.5% for "military-adjacent costs." This includes areas like cybersecurity, logistics, and dual-use goods.

All the changes are creating a frenzy among investors. The WisdomTree Europe Defence UCITS Fund (WDEF.L) is up more than 20% since it launched in March. Some are treating this moment like a generational tailwind for military contractors.

But not every European defense contractor will come out on top... despite what the market seems to think.

Rheinmetall (RHM.DE) is Europe's latest defense darling...

The German contractor is in the spotlight as investors rush to capitalize on a breakout moment. As Germany's top supplier of ground systems, Rheinmetall supplies armored vehicles, large-caliber munitions, and high-tech weapons systems.

With NATO gearing up for a record-breaking expansion, Rheinmetall seems like a perfect bet.

There's only one problem. This business has never delivered elite returns.

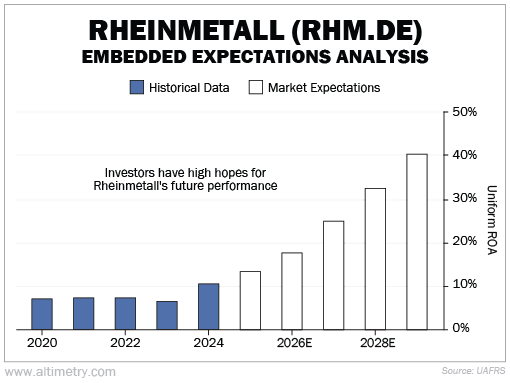

Rheinmetall has been around through periods of extreme geopolitical tension... like Syria in the late 2010s and Crimea in 2014. But Uniform return on assets ("ROA") hovered in the low single digits all that time.

Returns only cleared the 10% mark once between 2012 and 2023. And it took the threat of war on Europe's doorstep and ballooning military budgets for Uniform ROA to reach double digits again last year.

We see 2024's 11% returns as a new baseline for the company. But investors think this is just the beginning.

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA works a lot like a betting line in a sports bet... We use Rheinmetall's current share price to calculate what investors expect from future performance and compare those forecasts with our own.

It tells us how well our "team" (the company) has to perform to justify the market's "bet" (the current price).

Today's investors assume Uniform ROA will soar above 40% by 2029. That's nearly four times higher than Rheinmetall's best result yet.

Take a look...

Investors are looking for a near-perfect outcome.

Not only is this a lot to ask... it's also far above what's typical, even for top-tier defense contractors. Top U.S. contractor Lockheed Martin (LMT) has never returned more than 26% in a year.

And Rheinmetall has never come anywhere close, even during boom times.

NATO's new era will create plenty of opportunity...

But that doesn't mean every defense stock is a bargain.

Rheinmetall isn't about to become the Lockheed of Europe... no matter what investors seem to think. Until last year, it averaged returns of just 5%.

We don't blame folks for chasing the rearmament trade. There's a lot of money to be made here. But you need to be selective. Story and fundamentals are not the same.

Just because a company makes tanks... doesn't mean it's built to print cash.

Joel Litman

June 11, 2025