Leading memory and storage producer Micron (MU) announced a big change in December...

Leading memory and storage producer Micron (MU) announced a big change in December...

The company decided to wind down its flagging consumer business.

This includes reducing Dynamic Random Access Memory ("DRAM") and Solid State Drive production for smartphones and laptops.

It's shifting the focus to enterprise-grade memory... to accommodate massive AI build-outs.

Tech giants, like Nvidia (NVDA), Microsoft (MSFT), and Alphabet's (GOOGL) Google, need high-bandwidth memory ("HBM") to sustain massive AI clusters.

Together, their data centers are expected to consume 70% of all high-end DRAM in 2026.

But there's a caveat... Meaningful new supply won't arrive until at least 2028. And data centers, plus everyday consumers, will still need memory.

Today, we'll explain why these supply constraints are creating a rare opening for one of the smaller tech companies... while industry giants chase big data-center opportunities.

The memory space used to be 'boring'...

These tiny chips sat quietly inside smartphones, laptops, cameras, and game consoles. When you ran out of storage, you just bought more.

The AI boom has completely changed the landscape. The newest AI systems are hungry for HBM... like 3D-stacked DRAM technology.

And the "Big Three" memory manufacturers – Samsung, SK Hynix, and Micron – are all-in on this pivot...

Samsung is racing to triple its HBM sales by 2026 to keep pace with demand. SK Hynix's production capacity is fully booked through 2026. (It's backed by a $13 billion investment in the world's largest HBM assembly plant.) And Micron has already inked agreements to sell its entire 2026 HBM supply.

This isn't a mere inventory blip. High memory demand is pulling manufacturing away from consumer-oriented chips that keep smartphones and personal computers running.

And as major suppliers shift to AI, the consumer market isn't getting a clean handoff.

That's setting up a golden opportunity for companies that are willing (and able) to serve that market.

That's where computer-tech firm Sandisk (SNDK) comes in...

Its core business is flash storage – the kind that ends up in consumer devices. Sandisk also serves the enterprise space... without living and dying by it.

The company's memory sales for data centers make up 15% of revenue (up from 12% in the latest quarter). Its consumer and retail markets make up 85% of revenue.

That distribution matters. It lets Sandisk benefit from the AI memory trend while sticking to the consumer lanes that tech giants are abandoning.

The company also has a strong grip on intellectual property ("IP")... with a vast portfolio of memory patents, trademarks, and trade secrets.

These include flash memory and controller technologies, which are essential for both data centers and consumer products.

This IP framework allows Sandisk to protect and manufacture key memory technologies... and determine their pricing.

Despite its strong competitive advantage, investors still underestimate Sandisk's future potential...

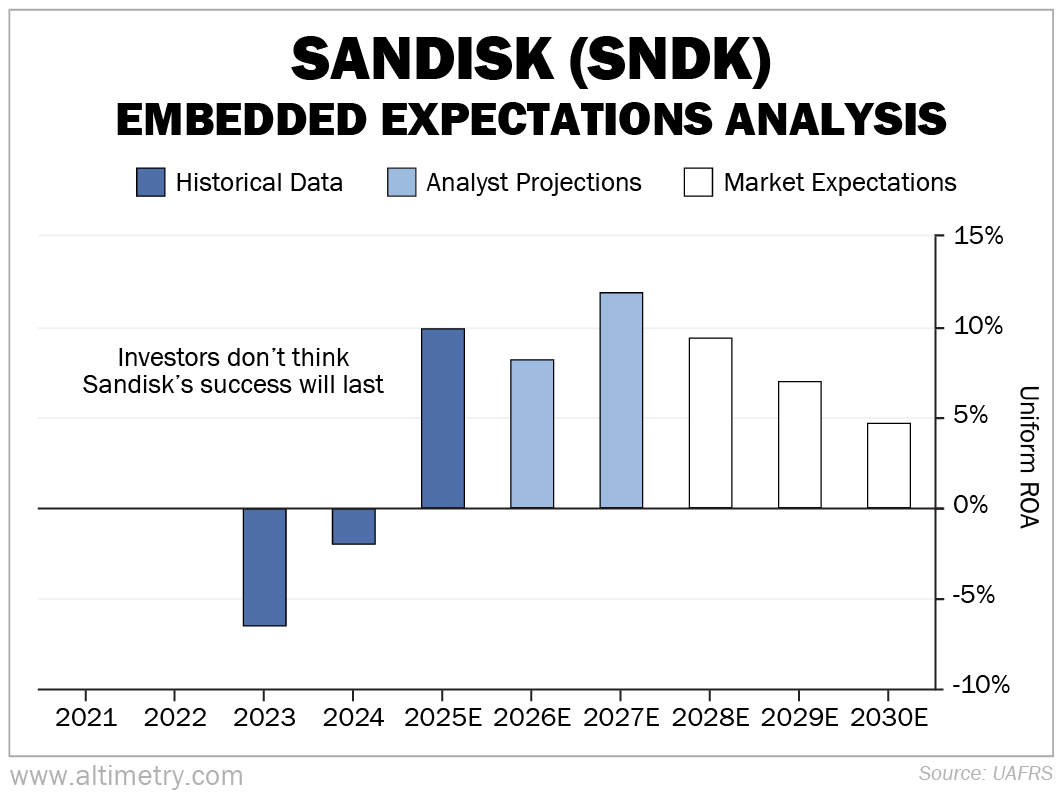

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

The SNDK stock is up a whopping 1,443% since spinning off of Western Digital last year. Yet investors are still downplaying Sandisk's success.

The company's Uniform return on assets ("ROA") hit 10% last year – just a bit below the 12% corporate average.

Wall Street analysts expect profitability to stay around that level for the next two years. And yet, investors expect its Uniform ROA to fall to just 5%. Take a look...

Investors are treating Sandisk's recent surge as a short-lived spike. But that doesn't reflect the company's true potential.

When companies like Micron step back from consumer products, someone else needs to step in...

And Sandisk is doing just that. It's leaning into the consumer-facing part of memory technology exactly when the tech giants are focusing on AI infrastructure.

Yes, data centers will continue expanding. But consumers will also continue buying smartphones and laptops. So both segments need a steady memory supply.

To succeed in that kind of market, companies need to do three things: One, keep the memory supply flowing across segments. Two, defend their market share. And three, avoid getting squeezed out by competitors.

Sandisk has the scale to accommodate everyday consumers and enterprise clients. It also has the IP muscle to keep store shelves from becoming too crowded with competing products.

Regards,

Joel Litman

March 4, 2026

P.S. Speaking of competitive advantage, Warren Buffett was a master at finding companies that outperformed the competition. My team and I have applied that same idea in analyzing more than 3,000 stocks. And there's one company that stood out. According to our research, it's the one stock Buffett himself would buy today if he could. Adding it to your portfolio could help you make a killing... but you need to act fast. Find out all the details here.