It might be time to revisit your budget...

It might be time to revisit your budget...

For most of the pandemic, the U.S. government found ways to keep money in consumers' pockets.

If you kept up with the headlines, you can probably recite the list by heart at this rate... Stimulus packages kept spending strong, companies happy, employment high, and interest rates low.

This is the opposite of what would happen in a recession. And while it propped up the economy for years, we're now seeing a key sign that the "easy money" era is over...

Starting October 1, student-loan payments will resume for almost 27 million borrowers. The average borrower owes about $400 per month. So many consumers will have to make some tough budgeting choices.

These folks haven't had to worry about student loans for the past three years, which means a big adjustment. Analysts anticipate more households could fall behind on credit-card and other loan payments as a result.

It's also worrisome for retail businesses. As folks have to spend more on debt repayments, they'll have less money for discretionary spending.

The macroeconomic environment is getting worse across the board. Today, we'll dive into further detail about this added obligation... and why it's stress to the already troubled U.S. consumer.

Consumer balance sheets were looking great...

And the same was true for corporate credit.

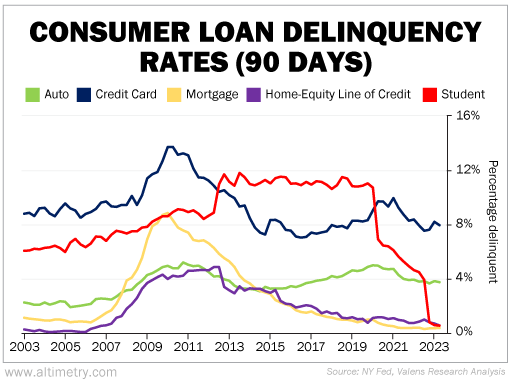

Starting in March 2020, when the government paused student-loan payments, delinquency rates started falling for almost every form of consumer credit. Many rates trended toward record lows.

For instance, credit-card delinquency rates fell from nearly 10% in mid-2020 to as low as 7.5% in September 2022. Auto-loan delinquencies fell from more than 5% to under 4%.

Student-loan delinquency rates fell the most. They had been above 11% for most of the 2010s. By late 2022, they had dropped below 2%.

Take a look...

Unfortunately, that trend couldn't last forever. Things are getting tougher for borrowers, including those with student loans.

Again, before the pandemic, more than 11% of student-loan borrowers were already more than 90 days late on their payments. Economists and Bank of America expect that pattern to pick right back up when the pause ends.

That will almost immediately add $167 billion in delinquent balances back to the U.S. economy.

Rising delinquency rates will put pressure on everything else...

When student-loan payments were halted, it drove delinquency rates down. So it makes sense that as those payments pick up, so will delinquency rates.

This is going to put pressure on the entire economy... It will send other types of loan delinquencies higher and hurt retail businesses.

Keep an eye on all kinds of consumer delinquency rates in the coming months. As they start rising, credit issues will worsen. We may even see the retail landscape deteriorate.

These are all signs that we're not out of the woods yet.

Regards,

Joel Litman

August 14, 2023