In the days after America's first strikes on Iran, different markets reacted quite differently...

In the days after America's first strikes on Iran, different markets reacted quite differently...

European markets panicked. Investors suddenly expected two interest-rate hikes from the European Central Bank by the end of the year.

U.S. markets stayed calm for the most part. They're still pricing in a few more Federal Reserve cuts... at least at first.

When oil prices jump, investors start thinking about inflation and the odds of an economic slowdown. Conflicts like this are typically a drag on the global economy, especially depending on where oil prices end up.

Still, this divergence in reactions was too wide to make much sense.

The same oil shock is hitting both sides of the Atlantic...

The same geopolitical risk is in front of everyone – at least, from an economic standpoint.

But Europe started trading like inflation was about to roar back and force policymakers into action... while the U.S. was still behaving as though nothing was amiss.

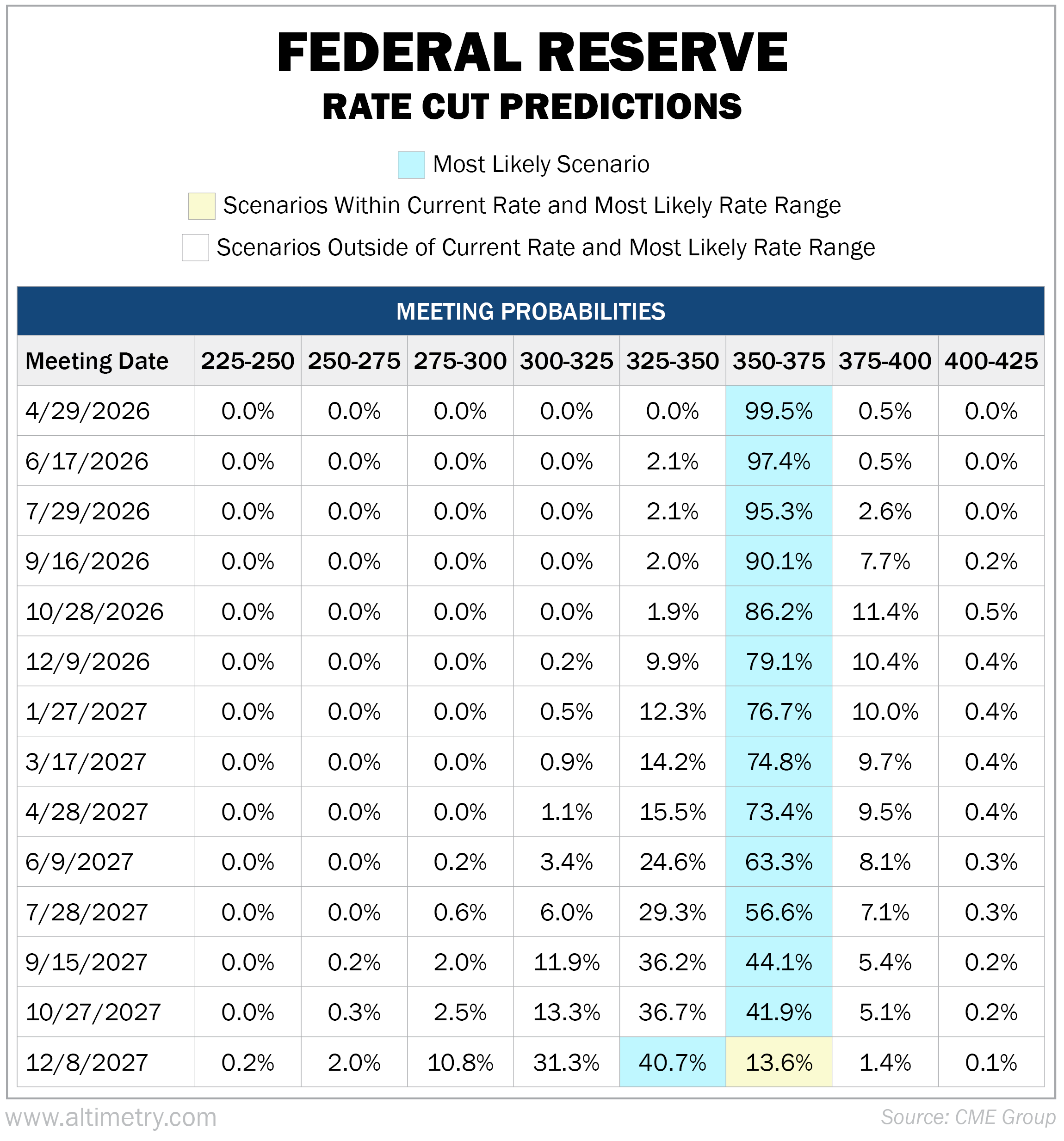

Longtime subscribers know we use the CME FedWatch Tool to check market expectations. It monitors futures contracts to estimate how likely the market thinks interest-rate hikes or cuts are.

Right now, CME FedWatch is predicting no rate cuts until December 2027. Take a look...

Europe has a similar tool called the ECB Watch. And as we said, it's calling for two rate hikes by the end of 2026.

That tells us European and U.S. investors weren't reacting to the same future. They were interpreting higher oil prices to mean two different things.

Europe has more reason to worry...

In general, the U.S. holds far more energy reserves than the European Union. That gives it much more protection from spikes in oil prices.

So America is far less exposed to a sudden jump in crude oil... because it can produce more of what it needs at home.

Europe doesn't have that same luxury. It remains much more dependent on imported energy. Rising oil prices act like a faster, heavier tax on growth.

That's why Nohshad Shah of Citadel Securities estimates that for every $20 rise in oil prices, the U.S. loses about 0.05% of its GDP... while Europe loses 0.19%.

In other words, Europe takes almost four times the hit the U.S. does from the same move in oil prices.

If your economy is more dependent on imported energy, you'll be more sensitive to a geopolitical shock that threatens oil supply...

That's natural. But current European market expectations still seem extreme.

Crude oil is surging above $100 per barrel. Shah believes this jump should only push European consumer-price increases from below 2% to roughly 2.3% by year-end.

That's certainly a rise in inflation. But it's not the kind of wave that should force the European Central Bank into a full tightening cycle.

The U.S. is in a similar boat. We've said many times that oil is the key to the future of the economy. The commodity influences everything from shipping to manufacturing to consumer sentiment.

But like with Europe, higher oil prices alone don't translate to a new tightening cycle for the U.S.

Investors are trying to guess central banks' next move...

And they're trying to do so before they know how long (or how bad) this oil shock will be.

For the U.S. in particular, after the invasion of Iran, the market shifted from expecting a more active cutting cycle to a holding pattern.

But that's not necessarily a bad thing. It tells us the market is looking for more information before getting ahead of itself.

Investors are waiting to see whether oil keeps climbing... and whether inflation actually follows.

If oil stabilizes, markets can move back toward rate cuts. If oil keeps surging, expectations can turn more hawkish in a hurry.

Keep a close eye on investor expectations through the CME FedWatch. This is one of the best ways to track how folks are interpreting the future... before the future fully arrives.

Regards,

Joel Litman

April 7, 2026