Bankruptcy is the ultimate black mark on a company's record...

Bankruptcy is the ultimate black mark on a company's record...

It spooks customers and employees and disrupts supplier contracts. It can also force parties into the courtroom... where a judge determines the company's fate.

That's why struggling businesses will try almost anything to avoid bankruptcy.

Over the past few years, many of them have turned to "liability management exercises," or LMEs. (These tend to involve "creditor-on-creditor violence," which we'll touch on later.)

The idea is simple. A troubled company cuts a deal with a group of lenders. Those lenders offer extra financing or tweak loan maturity dates. In exchange, they get priority when the debt becomes due.

This approach buys the company time and keeps equity afloat. It also helps management save face... They can say that the business "handled things out of court."

Luxury retail group Saks Global pulled off an LME just last year. Five months later, it still ended up filing for bankruptcy. Many companies suffer a similar fate.

Today, we'll explain why LMEs usually don't fix corporate problems. In fact, they often warn investors that time has run out.

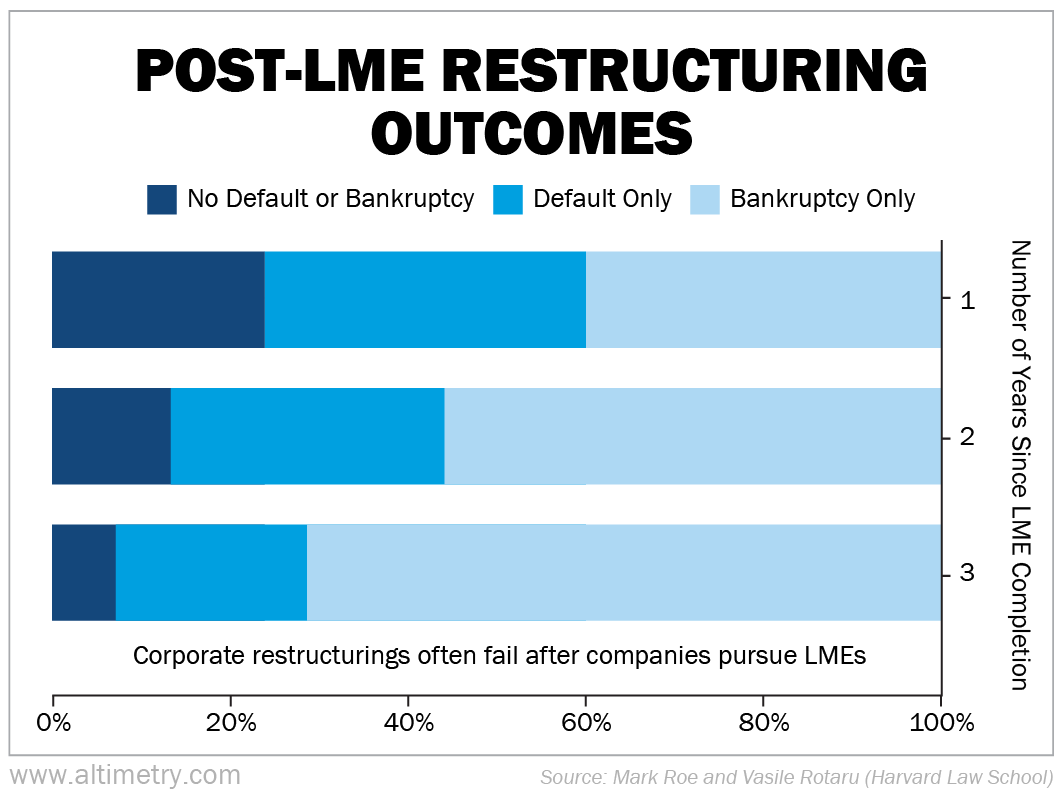

A recent study from Harvard Law School's Mark Roe and Vasile Rotaru confirmed this reality...

Roe and Rotaru built a dataset of 89 LMEs and tracked their outcomes. The results were brutal...

Within one year of completing an LME, roughly three-quarters of companies had a new default or bankruptcy filing.

After three years, just over 7% of companies had avoided bankruptcy or default. In other words, close to 93% failed to generally stay out of trouble, and about 71% ultimately filed for bankruptcy.

The average time to bankruptcy was about 17.5 months... The median was closer to 15 months.

Many investors believe LMEs create breathing room for change. In reality, they just prolong the inevitable.

The Roe-Rotaru study also shows why so many companies fail...

In most cases, LMEs don't reduce the debt owed. But they do increase the number of lenders (and, therefore, potential claimants). That goes back to the idea of "creditor-on-creditor violence" – where creditors battle each other in court to get paid.

A distressed company needs fewer obligations (not more)... and a simpler structure. That means converting complex, high-interest loans into equity and/or getting rid of competing lenders.

LMEs frequently deliver the opposite. They add fresh debt, raise interest rates (due to the high-risk borrower), and pit lenders against each other.

The rare wins create the illusion that LMEs work...

Yes, LMEs have helped some companies recover... like online used-car retailer Carvana (CVNA) and telecommunications firm EchoStar (SATS). Certain businesses have rebounded even after declaring bankruptcy... like General Motors (GM) and American Airlines (AAL).

But those are all exceptions to the rule.

Once a company has pursued an LME, you can safely assume three things...

One, the company needs money fast. Two, the easiest way to get that money is through a new lender. And three, the "extra time" an LME provides increases the debt burden and default risk.

All of that explains why so many struggling companies can't avoid bankruptcy. It also shows why these stocks often tempt investors...

With additional financing, companies keep their heads above water. And the handful of corporate turnarounds provide encouragement. But behind the scenes, creditors are fighting for scraps.

The bottom line is, LMEs rarely improve failing businesses. Beware of the false narratives that suggest otherwise.

Regards,

Rob Spivey

March 5, 2026