When COVID-19 started spreading, many people tried to stay in their own bubbles...

Folks avoided taking public transportation like buses and trains. Most restaurants shifted to "to go" operations. Many grocery stores restricted which way you could walk in aisles.

Heck, we didn't even want to touch any surfaces outside our homes – or even inside them, in many cases.

And of course, hospitals were some of the most dangerous places...

Dozens – if not hundreds – of new patients went in and out of these buildings every day. Most of these folks needed COVID-19 testing or treatments. And as a result, the needed precautions to treat these patients overran many hospitals' day-to-day operations.

Plus, in fear of getting sick, a lot of people avoided going to hospitals altogether if they could. They put off "preventive care" procedures for months – if not years.

But now, more and more folks are going back into the world...

And that means these people need to catch up on months of missed preventive-care procedures. By that, we're talking about things like shots and health-screening tests.

As we near the end of the pandemic, many hospitals are starting to feel its effects...

They're struggling to keep up with the growing demand for preventive-care procedures. And as federal funding programs end, they'll no longer be able to rely on these stopgaps.

To make matters worse, much of the preventive-care wave is coming from rural, largely uninsured communities. These folks often can't afford the real costs of treatment.

A strong 2021 might not have been enough for health care companies...

Most health care companies experienced a profitable 2021 in the wake of the pandemic.

Federal programs paid for people who couldn't afford treatment. And that kept hospital finances flowing.

A notable example is Community Health Systems (CYH)...

Community Health is among the largest hospital owners in the U.S. The company mostly focuses on rural hospitals – the same ones that will soon be inundated with preventive-care procedures that folks can't afford.

Back in 2014, Community Health was the country's largest provider of general health care services. It operated around 200 hospitals. However, it has suffered in recent years. As a result, it only operates 83 hospitals today.

The problems could've been even worse for Community Health, too...

Unpaid patient bills surged during the pandemic. But fortunately, it collected more than $700 million in COVID-19 relief funds from the federal government to keep the lights on.

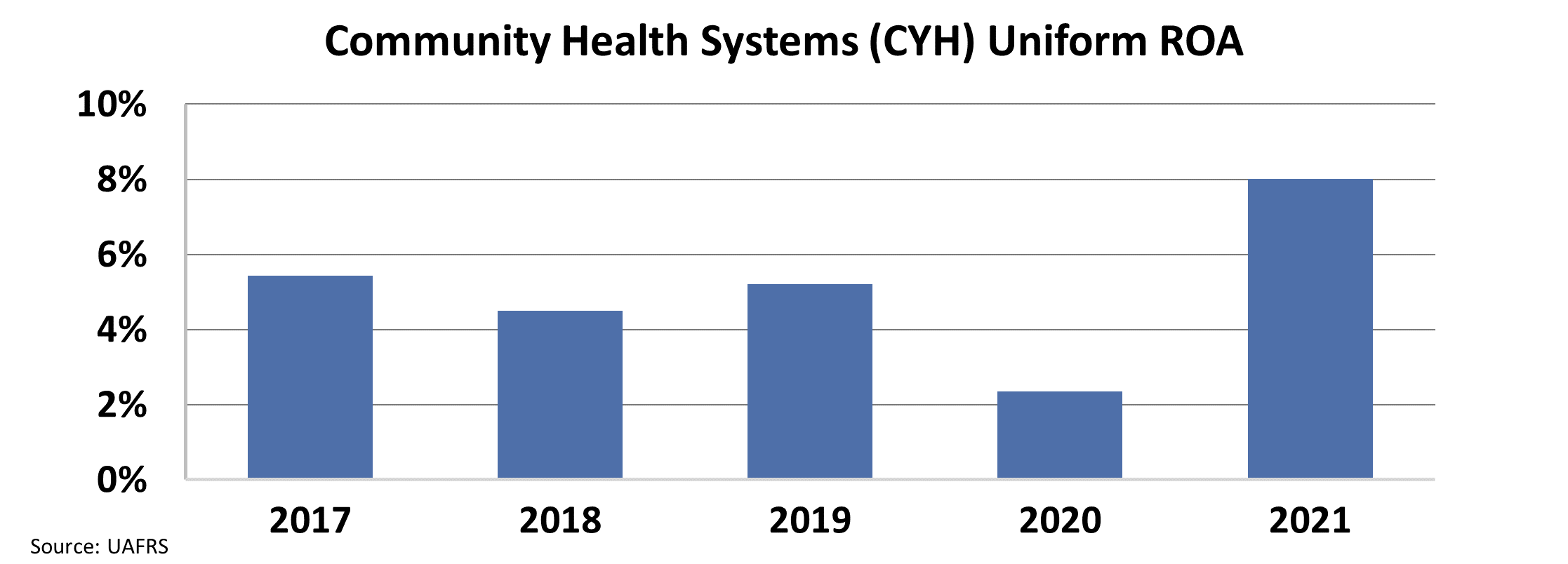

After Community Health's Uniform Return on Assets ("ROA") plummeted to roughly 2% in 2020, it had its best year in five years. Its Uniform ROA surged to 8% in 2021...

This increase likely isn't sustainable, though. As we discussed, a surge of preventive-care treatments is coming... And fears are growing that they won't be profitable.

These problems could lead to serious cash-flow issues for hospitals in the near future.

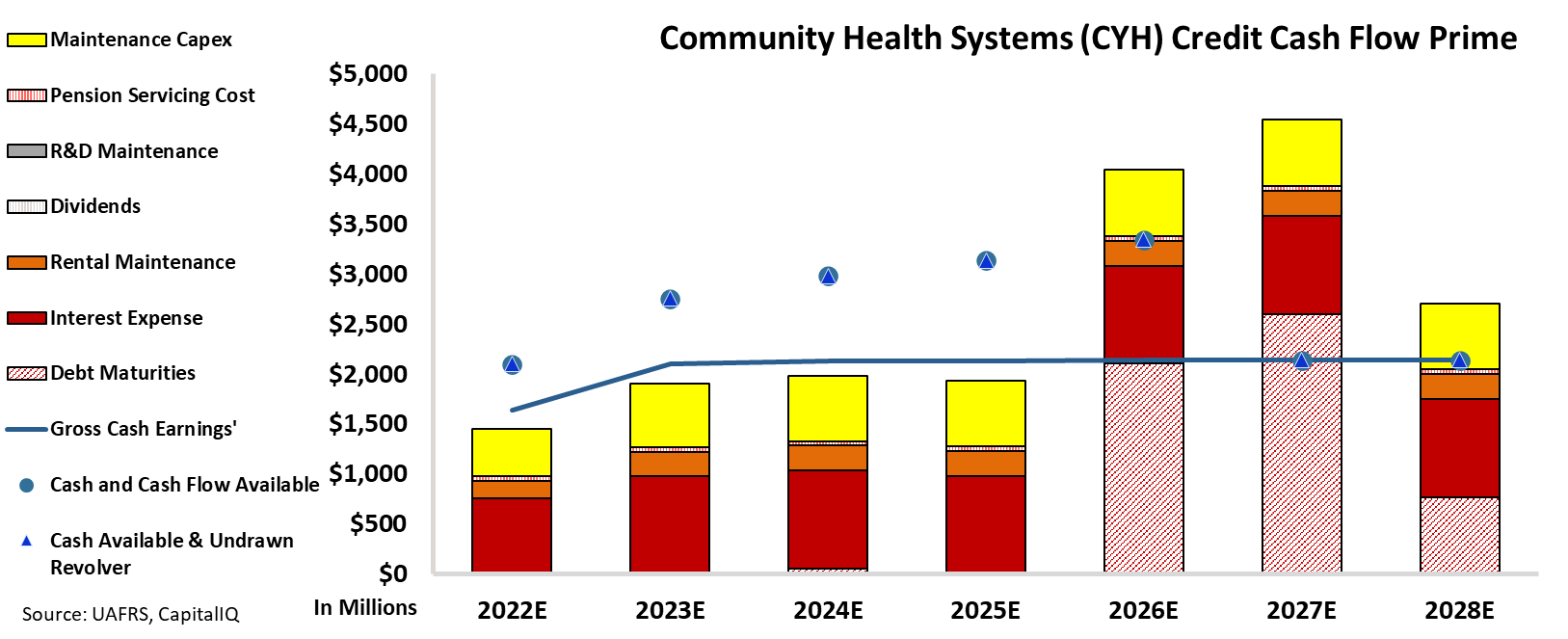

Using our Credit Cash Flow Prime ("CCFP") analysis, we can get to the heart of Community Health's true credit risk...

In the below chart, the stacked bars represent the company's obligations each year through 2028. Then, we compare these obligations to its cash flow (blue line), as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

Community Health's CCFP analysis shows that the company's gross cash earnings will just meet its operating obligations in the next three years. However, as you can see, they aren't enough to cover the huge debt maturities in 2026 and 2027...

As the CCFP analysis highlights, Community Health will struggle in a few years to pay off its debt. And that's even before accounting for a further constriction of cash flows from the expected preventive-care bottlenecks in rural hospitals over the next few years.

In a situation where Community Health can't maintain its profitability, it may have a tough time paying off its operating obligations or investing in future growth. And in turn, that exposes the business even further to its huge debt headwalls in 2026 and 2027.

All of these facts make the company's credit and capital structure risky and speculative.

Thanks to Uniform Accounting, we can see more than just which bonds to avoid. We can also see which stocks may be dragged down as well – like Community Health.

When COVID-19 started spreading, many people tried to stay in their own bubbles...

When COVID-19 started spreading, many people tried to stay in their own bubbles...