In 2024, Swedish fintech company Klarna used its AI assistant to replace 700 customer-service agents...

In 2024, Swedish fintech company Klarna used its AI assistant to replace 700 customer-service agents...

And, as expected, the market went haywire...

Customer-service stocks plunged. Debt prices collapsed. Creditors geared up to collect bankruptcy assets. And industry giants faced uncomfortable questions about their future.

The damage is now undeniable... Call-center leader Teleperformance's (TEP.PA) shares have fallen to their lowest level since 2016.

Meanwhile, competitors like KronosNet, Foundever (formerly Sitel), and Transcom are restructuring, raising capital, or shutting down units altogether.

AI isn't just making customer-service lines more efficient... The technology is dismantling the entire industry.

Yet AI might be the very thing that saves it.

As this technology rapidly transforms call-center businesses, we'll explain why the market is pricing in a bleak future... even for the biggest names.

AI can now handle thousands of customer interactions per second...

And with none of the payroll, training, or turnover issues that come with human labor.

That's why Klarna's strong move toward AI wasn't a one-off... It was a warning shot. Call centers are undergoing big changes around the world...

Foundever is restructuring its distressed loan debt. And Transcom has closed two units in Germany... Its notes have fallen to 78 cents on the euro, indicating a bankruptcy risk.

In response, private-equity sponsors are injecting emergency capital and pushing hybrid models – part AI, part human – in the hope of salvaging value.

KronosNet, for example, raised €75 million in equity and matched that with new debt to double down on AI initiatives.

However, these efforts may not be enough, as even the largest operators are under strain.

The customer-service industry is breaking down much faster than it's finding solutions...

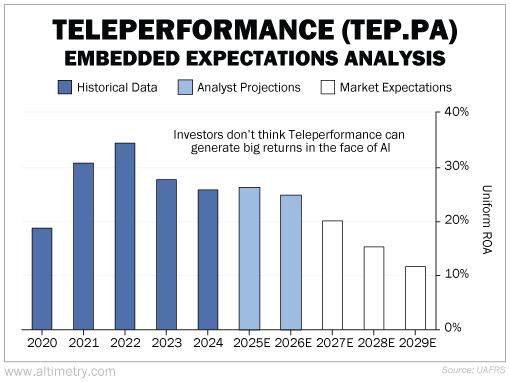

Right now, investors are pricing in an industry decline. And we can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Teleperformance's Uniform return on assets ("ROA") shot up from 19% in 2020 to 34% in 2022. This was largely driven by the shift to remote solutions during the COVID-19 pandemic.

However, its Uniform ROA fell to 26% in 2024, as AI began taking over call centers. The market is expecting profitability to fall even further, to about 12%, by 2029.

Take a look...

Most of Teleperformance's revenue comes from services that can now be automated. And given the current AI surge, the market estimate seems fair.

Yet, AI is much more than a way to boost productivity and efficiency...

It's an existential threat to customer service as a whole... And investors are starting to take notice.

However, this technology has become an essential tool. Businesses that don't embrace AI are trading on borrowed time.

Some are faltering even with investments in this space... Teleperformance, for example, has pledged €100 million for AI partnerships. Yet its stock has plunged more than 70% from its late-2021 peak.

The bottom line is, AI integration is a process. And unless these companies reinvent themselves, in tandem with AI, they won't survive.

For now, steer clear of traditional call-center businesses... Focus on companies that emerge as leaders in the adoption of AI or hybrid models.

Regards,

Rob Spivey

April 3, 2025