Activist hedge fund Starboard Value shows up when good businesses begin to stumble...

Activist hedge fund Starboard Value shows up when good businesses begin to stumble...

It has already helped improve companies like restaurant operator Darden Restaurants (DRI) and e-commerce leader eBay (EBAY).

Now, it has a new target... software company Dynatrace (DT).

This firm equips information-technology teams with automated, AI-driven insights that help with troubleshooting.

But Dynatrace is still caught in a brutal spot... Investors have been dumping software companies left and right as AI continues raising fears about competition.

Dynatrace's shares are down more than 30% since last June and more than 15% year to date. That happened after the company built a leading position in a mission-critical software market.

Now, investors are wondering if Dynatrace can make the changes it needs to fully lean into AI. If so, it might be able to join Starboard's list of successful turnarounds.

AI isn't as much of a threat to Dynatrace as the market suggests...

Dynatrace sells "observability" software. In plain English, these products help large companies monitor their applications, cloud systems, infrastructure, and software tools.

When something breaks, slows down, or behaves strangely, observability platforms help identify the cause.

Application performance monitoring ("APM") is the biggest part of that segment. Starboard calls Dynatrace the clear leader in APM and says its end-to-end platform is built for corporate AI use.

As companies deploy more AI agents and automated workflows, their systems are creating more vulnerabilities. They're also generating a lot of data. Dynatrace ingests that data, interprets it, and helps companies act fast when problems arise.

Starboard also points to Dynatrace's Davis AI engine, which has been part of the platform for nearly a decade. It uses AI technology to fix problems safely and quickly.

Dynatrace also has a strong pricing model... Roughly 70% of its annual recurring revenue comes from its Dynatrace Platform Subscription ("DPS")... This provides access to both the APM platform and the Davis AI engine.

Starboard thinks Dynatrace is wasting this strong foundation...

And it's targeting two areas of the business – the sales organization and its research and development (R&D) arm. Dynatrace's ability to drive revenue through sales trails that of its peers. And the company's new product launches have historically missed revenue targets.

As a result, revenue growth has slowed down... Dynatrace posted annual recurring revenue growth of 25% in the first quarter of 2024. That fell to just 17% in the fourth quarter of 2025.

Starboard's bigger complaint is profitability...

Typically, once software companies get enough customers on board, profitability skyrockets to compensate for slower growth.

But Dynatrace's adjusted operating margins barely moved between 2021 and 2026, from 29.5% to 29.2%.

Dynatrace is massively undervalued, but it could easily recover...

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

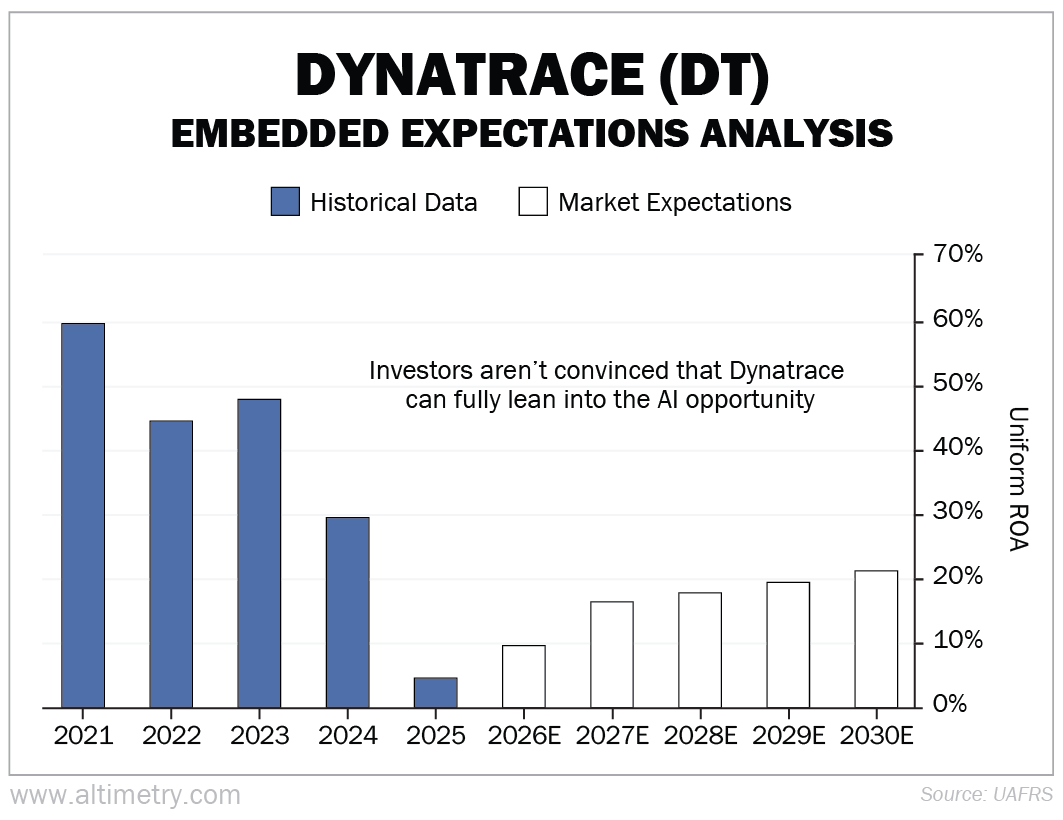

Dynatrace was quite profitable between 2021 and 2024, with a Uniform return on assets ("ROA") between 30% and 60%. But in 2025, its Uniform ROA tumbled to just 5%.

Investors don't seem to think it'll stay that low. But they don't expect it to fully rebound, either. The market thinks Dynatrace's Uniform ROA will settle around 21%. Take a look...

If Dynatrace can implement Starboard's advice and prop up struggling margins, investor expectations could prove to be way too low.

Dynatrace doesn't have to do much to turn itself around...

Starboard is pushing for practical changes.

It wants Dynatrace to cut the bloat in sales and make smarter R&D investments. None of that requires reinventing the business.

Lowering sales and marketing costs would bring Dynatrace in line with its peers... and boost profitability.

The company already has a solid AI-powered platform... The Davis AI engine has been running for nearly a decade. And its DPS model ties revenue directly to customer usage and growth.

If management implements Starboard's suggestions, Dynatrace could more than double its free cash flow per share by fiscal year 2029.

Simply put, the company's fortune could change quickly. And investors who get ahead of that shift could make a killing.

Regards,

Joel Litman

May 1, 2026