When the AI revolution took off, hyperscalers rushed to get their graphics processing units, servers, and networking gear to market...

When the AI revolution took off, hyperscalers rushed to get their graphics processing units, servers, and networking gear to market...

That pushed chipmakers like Nvidia (NVDA) into the spotlight. And investors rushed in to profit from the trend.

Now, the pressure is shifting to another critical part of the AI build-out...

AI data centers need electricity. And electricity relies on power-generation equipment.

To produce electricity on a large scale, you need specialized turbines. Those take years to build... Turbine delivery timelines now stretch beyond 2029.

U.S. spending patterns are reflecting this new focus on power generation...

The cost of this equipment for data centers may soar to $65 billion by 2030... up from $2.6 billion in 2025. Total U.S. spending on power-plant equipment may ultimately reach a staggering $215 billion.

That's pulling industrial supply chains, plus three dominant turbine producers, right into the AI trade.

Data centers used to make up a sliver of the power-equipment market...

In 2020, they accounted for less than 2% of demand. Consulting firm McKinsey expects that to reach 12% by 2030.

Grid-connected data-center capacity is projected to nearly quadruple over the next four years. All of that growth is overwhelming the electricity-planning process...

Data centers requiring about 183 gigawatts ("GW") of electricity have already signed agreements with utility companies. Projects requiring 600 GW of power are still trying to pin down their supply.

Gas turbines are essential in securing that power. And, importantly, they can provide data centers with electricity around the clock.

Right now, all eyes are on three turbine producers that dominate the industry... GE Vernova (GEV), Siemens Energy (SMERY), and Mitsubishi Heavy Industries (MHVIY).

Historically, these companies formed a decent niche. Today, they hold the keys to the entire industry...

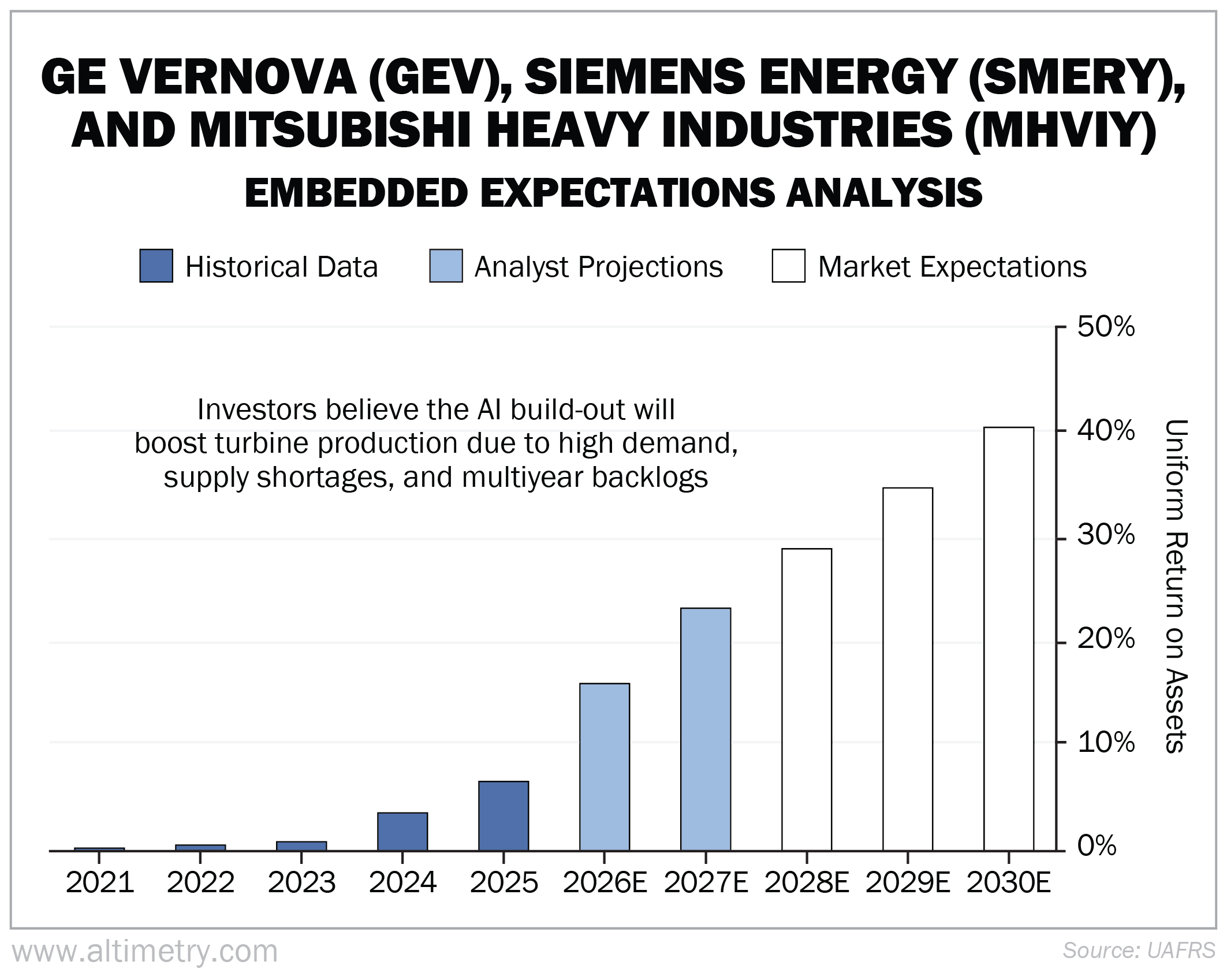

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

We've combined the EEAs for GE Vernova, Siemens Energy, and Mitsubishi Heavy Industries to illustrate the industry-wide trend. As you can see, they haven't been particularly profitable...

As recently as 2021, the companies averaged a Uniform return on assets ("ROA") of zero. By 2025, it reached an average of 7%.

That being said, Wall Street expects their average Uniform ROA to rise to 23% by 2027. (See the light blue bars below.) Investors are much more optimistic and expect profitability to reach 40% by 2030. Take a look...

That tells us investors are pricing in a major ramp-up in turbine-generated power.

The power bottleneck is already crowning the industry's winners...

Today, data-center developers, utilities, and power producers are all chasing the same turbine slots.

And companies like GE Vernova, Siemens Energy, and Mitsubishi Heavy Industries are taking center stage. (GE Vernova and Siemens are up 175% and 26% year over year.)

All three have better pricing power, stronger visibility, and a clearer earnings path than most industrial-equipment companies.

A spending surge is underway to fulfill the massive AI power demand. And with every new data-center announcement, turbine producers are building momentum.

The AI revolution started out with chips. Now it needs turbines. Investors who recognized that shift early are already being rewarded.

Regards,

Joel Litman

May 6, 2026