Something unusual just happened... Stocks got cheaper without breaking the economy...

Something unusual just happened... Stocks got cheaper without breaking the economy...

You probably don't need us to tell you that the past few months have been choppy.

Headlines out of the Middle East have driven volatility higher. And sentiment has stayed defensive as a result.

Last month, we argued that oil would dictate the market's next move. That remains true.

We still don't know how the Iran conflict will play out. It would be foolish to pretend we do. But so far, the most important market signal is that oil has fallen from recent highs.

After peaking around $120 per barrel following the invasion, Brent crude oil prices (the international standard) are hovering around $110 per barrel. That's well below the levels that would drive a recession, as we touched on in April.

So instead of worrying about oil, which seems to have largely stabilized... let's look at what's actually changing.

We now have official fiscal 2025 data from across the market...

Nearly every company has reported its 2025 earnings. And we've been able to run those results through our Uniform Accounting framework.

That gives us a clearer starting point for 2026 expectations. And the picture is stronger than many investors realize...

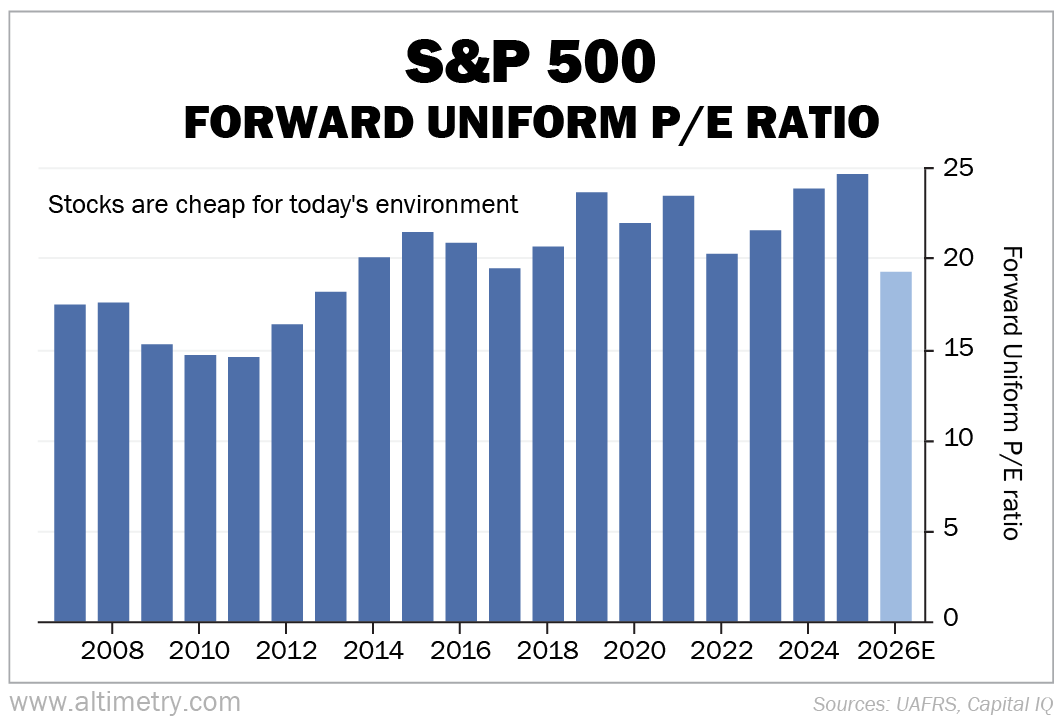

Valuations were already decent. The forward Uniform price-to-earnings (P/E) ratio was roughly 24 times last year – in line with our expectations, given today's level of corporate taxes, inflation, and earnings growth.

Based on 2025 results, we now expect roughly 19% earnings growth in 2026, well above the corporate average growth of 10%. Profits are still accelerating. Companies continue to spend and invest. And the earnings engine behind this bull market is chugging along.

Thanks to those stronger earnings expectations, the forward Uniform P/E ratio has fallen below 20. That's low for a market with solid profit growth, a supportive tax backdrop, and inflation that – outside of energy – remains manageable.

Take a look...

This is the part investors often miss. Valuations don't always fall because something breaks. Sometimes they fall because prices stall... while earnings improve.

We're seeing that setup right now...

And it's perfect for today's market.

Despite improving fundamentals, sentiment hasn't caught up. The market is still reacting to March's Iran-driven volatility.

But we're still seeing strong and accelerating earnings growth. That can keep powering the market forward. And with lower valuations, we have a good buying opportunity today.

There may still be some near-term headline risk from the Middle East. But we remain bullish.

This isn't what the start of a bear market looks like.

Regards,

Rob Spivey

May 4, 2026