These tiny silicon chips power all the devices and electronics we take for granted every day. And the pandemic only accelerated our reliance on semiconductors... Demand shot through the roof as the world moved to remote work and school.

But supply-chain shortages and heightened demand have made the critical components hard to come by. It doesn't help that the U.S. produces just 10% of the global chip supply.

Back in January, a Washington-based think tank called the Center for a New American Security conducted a war-game scenario studying our reliance on foreign chips. It also highlighted how that dependence could pull the U.S. into global conflict.

Taiwan produces more than 90% of the world's most advanced chips. And geopolitical tensions have people worried about what would happen if the country stopped production.

Since Russia invaded Ukraine, China has appeared even more likely to finally attempt an invasion of its own in Taiwan. But even without an invasion, China could seize Taiwan's semiconductor industry with just the threat of force. That would put a massive dent in the domestic and global chip supply.

To mitigate that risk, Congress has put out new bills aimed at bringing semiconductor production back to the U.S. This would help diversify the supply chain. But for investors, it also raises questions about what it means for current leaders in the space.

We can answer those questions by looking at one of the largest semiconductor makers through the lens of Uniform Accounting...

Taiwan Semiconductor Manufacturing (TSM) is one of the biggest players in the global chipmaking space. It sells to the largest electronics companies, like Apple (AAPL) and Nvidia (NVDA).

For years, Taiwan Semiconductor has dominated the industry.

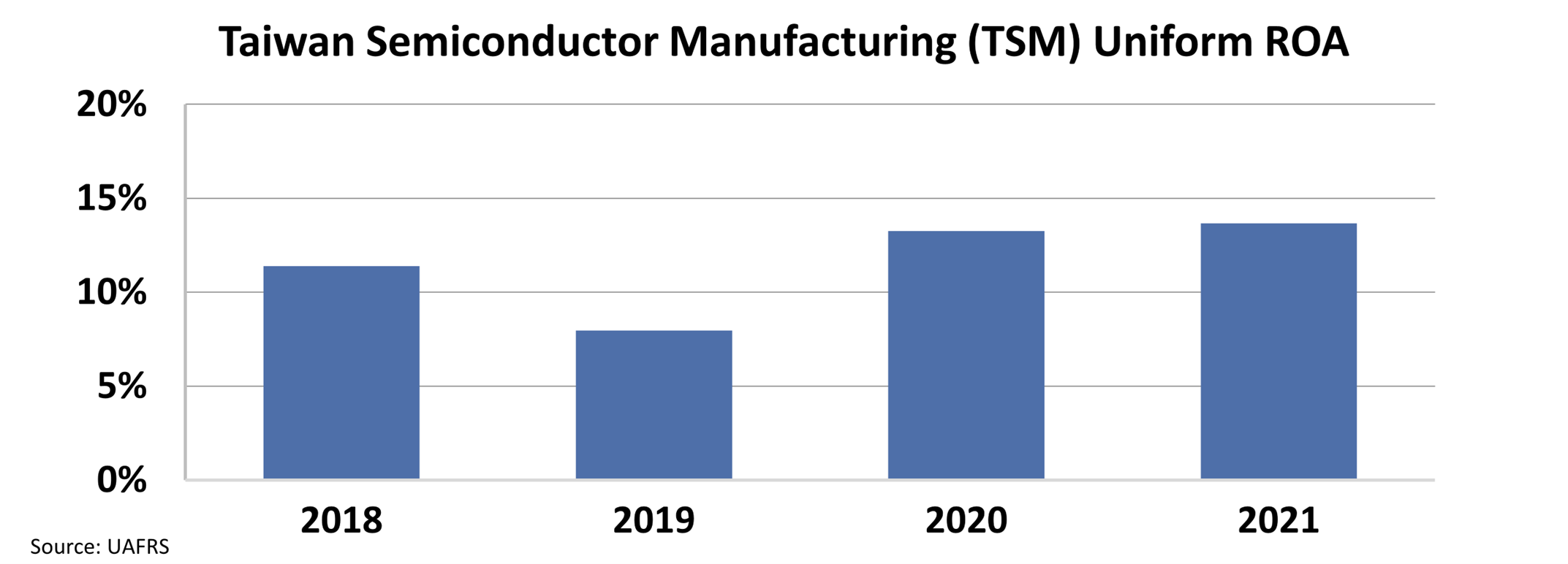

Its Uniform return on assets ("ROA") fell from 11% in 2018 to 8% in 2019 as it worked to expand capacity. But that drop was just a minor blip. Demand skyrocketed in 2020, and ROA rose to 13% and 14% in 2020 and 2021, respectively.

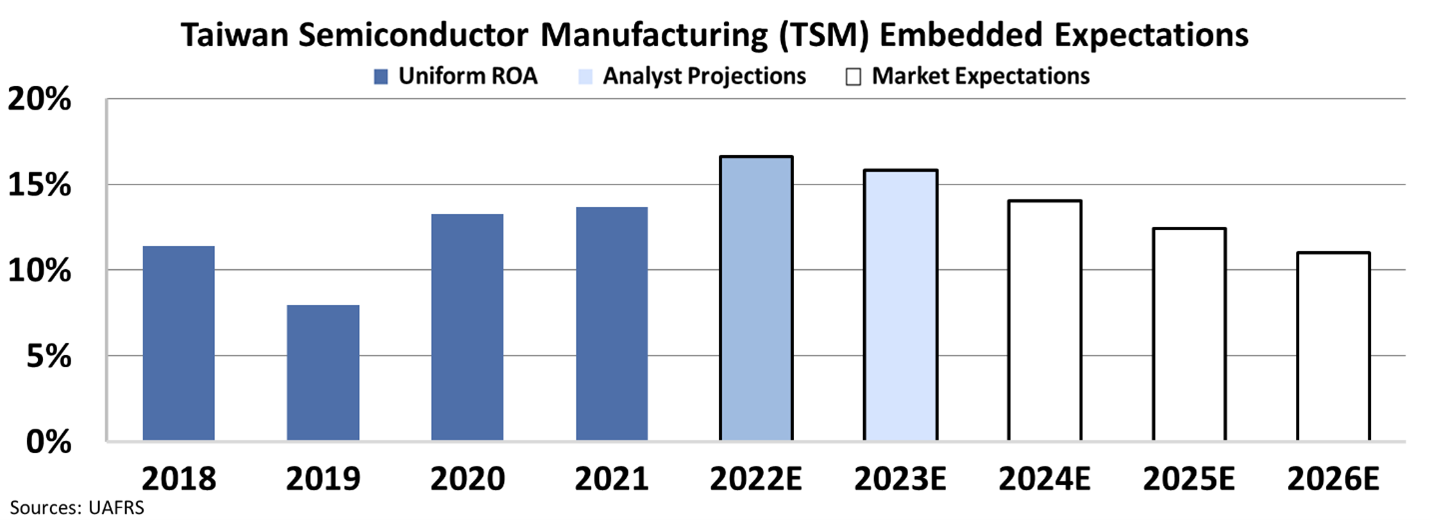

Analysts expect this improvement to continue. They project Taiwan Semiconductor will see ROA of 17% by 2023.

But our Embedded Expectations Analysis ("EEA") chart can show us what the market thinks of these forecasts.

As we often write, stock prices aren't driven by performance. They're driven by changing expectations. Said another way, a "good" company could be a terrible investment... while a struggling company could lead to huge upside.

Wall Street loves to use simple ratios to determine if a stock is cheap. But we understand the importance of market expectations...

If a company can do significantly better than the market anticipates, it could be priced cheap today. On the flip side, if the market expects greatness and the company doesn't deliver, its price will likely fall from current levels.

The following chart shows Taiwan Semiconductor's historical ROA (the dark blue bars)... Wall Street analysts' expectations for the next two years (the lighter blue bars)... and the market's ROA expectations for the next five years (the white bars).

As you can see, the market expects Taiwan Semiconductor's ROA to fall to 11% by 2026.

The market is pricing in increased competition as the U.S. prepares to bring more production onshore.

But investors may have jumped the gun...

Sure, as a country, Taiwan has dominated the space for years. And it has much more advanced manufacturing capabilities than the rest of the world. It will take years for domestic manufacturers to catch up.

But thanks to Uniform Accounting, we can see what the market really thinks about Taiwan Semiconductor. Investors' low expectations mean the company is actually cheap. Its Uniform price-to-earnings ratio is just 16.5 times.

Investors are running from Taiwan Semiconductor. But the company still has strong upside potential. Electronics aren't going anywhere... And demand for chips doesn't seem to be slowing down anytime soon.

The U.S. is working diligently in the background to build chipmaking capacity. But in the meantime, Taiwan Semiconductor will continue churning out chips – and strong returns for investors.