A few bad blows can wreck a food story fast...

A few bad blows can wreck a food story fast...

Salad-restaurant chain Sweetgreen (SG) was supposed to be one of the cleaner, fresher winners in fast-casual dining.

For a while, investors bought into that vision... When the company went public in 2021, it was valued at $5.7 billion. Today, however, it's only worth around $680 million.

That's because Sweetgreen has hit stumbling block after stumbling block since then...

Back in 2022, it suffered a lettuce shortage that caused its prices to skyrocket. One year later, its packaging supplier hit a financial snag and wasn't able to deliver its bowls – leading to another surprise price hike.

Customers noticed that costs were rising. At the same time, many folks reported a decline in food quality... which left them feeling the salads were no longer worth the price.

Over the past year, Sweetgreen's stock has fallen about 80%. It's now trading at a new all-time low.

Today, we'll look at whether Sweetgreen's brutal stock collapse has created a real turnaround opportunity... or whether investors should just give up on this struggling restaurant.

The pandemic hit Sweetgreen hard...

The salad chain built much of its business around folks who work corporate jobs. Many locations are in financial districts and other business-heavy areas.

But the COVID-19 pandemic shut off a year's worth of demand for office lunches.

The end of the pandemic should have been Sweetgreen's saving grace. Unfortunately, that's when lettuce and bowl shortages and food-quality issues hit.

The subsequent cost increases pushed customers away. Competitors like fast-casual Mediterranean restaurant Cava (CAVA) have since captured far more enthusiasm.

Cava went public two years after Sweetgreen at a similar size... but now it's worth about $10 billion (versus Sweetgreen's $680 million).

Sweetgreen has posted lower sales growth than Cava in all but one of the past 10 quarters. And its same-store sales deteriorated in 2025... from a 3% loss in the first quarter to a 12% loss in the fourth quarter.

The real issue here is that Sweetgreen never built a profitable foundation...

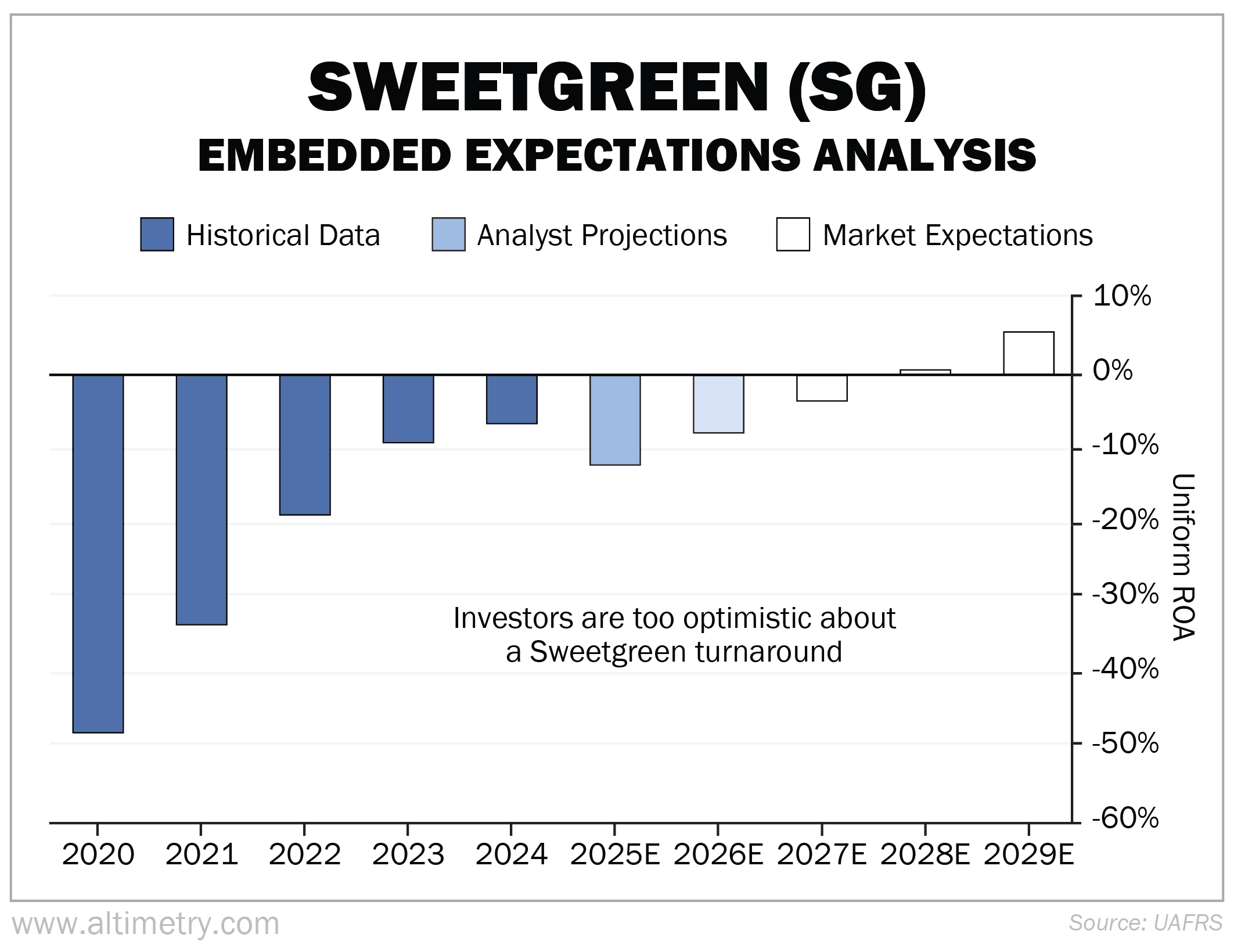

It was already on shaky ground before growth started to fade. In fact, the company has lost money every year since 2019. Uniform return on assets ("ROA") has never been higher than negative 7%.

And yet, investors are still holding onto a bit of hope. We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Alongside our EEA framework, we also like to look at near-term Wall Street expectations (the light blue bars). Analysts tend to have a pretty good grasp on where companies are headed in the next year or two.

Sweetgreen's sales are slowing. It's not doing much to get customers excited about its food. Wall Street analysts expect returns to drop to negative 12% when 2025 numbers are finalized.

And even though they think Uniform ROA will "improve" to a mere negative 8% in 2026, that number will still come in below the company's "best" year ever.

Wall Street clearly understands that Sweetgreen is an unprofitable business. But investors aren't so sure.

Despite the stock taking a beating, folks think Sweetgreen can right the ship... turning profitable by 2028 and reaching a record 5% Uniform ROA by 2029.

Take a look...

Keep in mind... the corporate average Uniform ROA is 12%. It's not like the market's 5% expectations are that high.

But they're still too high for Sweetgreen.

This business hasn't proved it can clear that 5% hurdle. It hasn't figured out how to turn a profit after nearly five years as a public company. And competition is heating up, making it hard for Sweetgreen to stay relevant.

Food is a fickle business...

Sweetgreen once looked like a category-defining concept. But today, it looks more like a reminder of how hard it is to scale a premium restaurant brand.

After repeated mishaps, this business is struggling to get back on track. And it's still not profitable.

There are always exceptions. A handful of fast-food giants have come out on top, thanks to a combination of consistency, customer loyalty... and a little bit of luck.

We doubt Sweetgreen will ever be one of them.

Regards,

Joel Litman

March 17, 2026