Elon Musk's latest triumph is almost upon us...

Elon Musk's latest triumph is almost upon us...

SpaceX is set to make waves when it goes public in just a few short days. It's expected to raise $75 billion at a total valuation of nearly $1.8 trillion... both record figures for a first-time IPO.

And SpaceX didn't stop there. An estimated 30% of shares could be set aside for retail investors on day one. That's far above the typical range of 5% to 10%.

Put simply, this isn't just one of the most-followed IPOs in history – or the biggest (although it is both of those things).

It's also the IPO with the most participation from individual investors. Even if you're not planning to buy in, chances are, you know someone who is.

We've spent the past two days doing an in-depth review of SpaceX's financials. In part one, we broke down the profitability of each business unit. And part two covered what we think those units should be worth based on what we know today.

Today, we'll put it all together – using two of our favorite Uniform Accounting tools to evaluate SpaceX's stock as a whole.

SpaceX has two profitable segments...

The space business earned a Uniform return on assets ("ROA") of 12% last year, right around the market average. We explained yesterday that it could be worth about $125 billion if it stood on its own.

And the satellite business (also called Starlink) is the company's cash cow, with 30% returns. We think Starlink should be worth as much as $600 billion.

SpaceX's third segment, AI, is losing money as it desperately spends on new data-center construction. Its Uniform ROA was negative 18% last year. And while it's hard to value an unprofitable business, we assigned it a best-case-scenario value of $600 billion as well.

All told, that puts SpaceX at a $1.3 trillion value by our estimates. That's quite a bit lower than its projected IPO valuation of $1.8 trillion.

That tells us expectations are high. And to understand just how high, we turn to the first of today's Uniform Accounting tools – the Embedded Expectations Analysis ("EEA") framework.

Longtime Altimetry readers have likely seen us throw the term 'EEA' around...

The EEA is a way for us to tell how well a company needs to perform in the future to be worth what the market is paying for it today.

Most Wall Street analysts use what's called a discounted cash flow, or "DCF" model. They add up their projections for all future cash flows... and discount them based on the "cost of capital." That just means how much money a company will have to spend to generate those cash flows.

That's how normal DCFs work. They're built on analyst assumptions.

There are a lot of investors combing over companies' earnings. For most companies... the market gets it right.

(That's why we don't recommend 1,000 companies here at Altimetry. Big-upside opportunities don't grow on trees.)

With our EEA framework, instead of coming up with our own assumptions, we start by assuming the market knows best. We use Uniform ROA and Uniform asset growth because they're an easy way to model free cash flow.

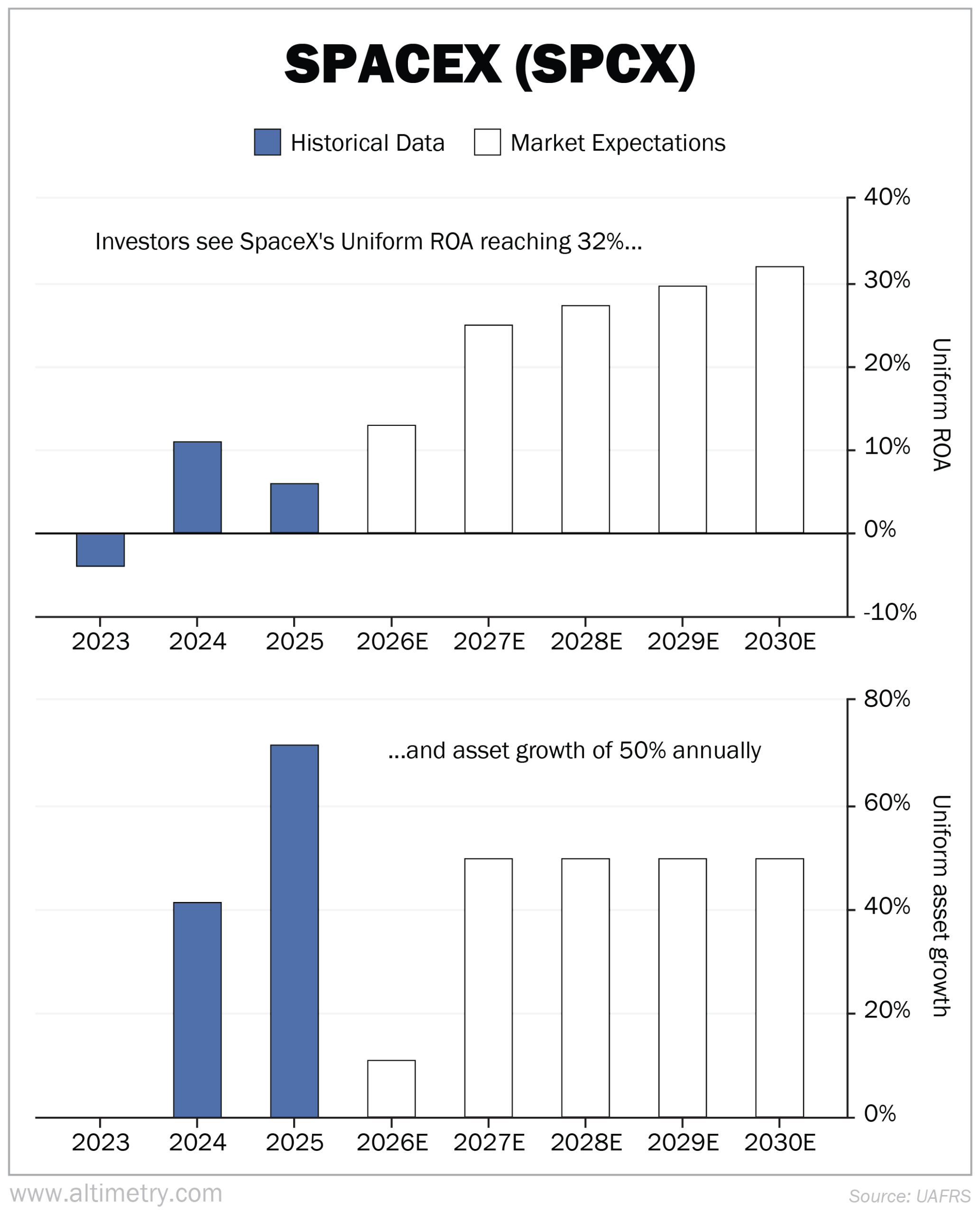

At a $1.8 trillion valuation, investors are betting SpaceX will generate returns of 32% by 2030. That translates to a staggering 660% growth in assets (50% per year for five years).

Take a look...

Based on those projections, the market expects SpaceX to have nearly $300 billion in assets... and to have generated roughly $100 billion in free cash flow by 2030.

That's what the company must achieve in order to satisfy investors.

We've spent the past few days explaining why that's possible. Starlink is well on its way to recording Uniform ROA of 60%. And the AI business strives to be like the hyperscalers, which averaged 29% returns last year.

But these are still goals. SpaceX's business isn't there yet. So we'd call its current valuation "aspirational."

And that brings us to the last piece of the puzzle. It doesn't matter what the company should do... unless management is prepared to do it.

We love an acronym here at Altimetry...

And when it comes to compensation, our favorite is "IDB" – or "incentives dictate behavior."

IDB is a pretty simple concept. It just means that people will do what they're paid to do.

No stock analysis is complete without a look at how management gets paid.

Read that again. We're not talking about how much management earns. We're talking about how leadership is being compensated.

To receive any stock awards from SpaceX, Elon Musk needs to grow the market cap to a massive $7.5 trillion. That's roughly 50% larger than "Mag Seven" darling Nvidia (NVDA)... which is currently the largest company in the world.

On top of that, Musk has two non-financial goals...

- Establish a colony on Mars with 1 million residents (if he hits this, he's entitled to 200 million additional shares of the stock)

- Launch enough data centers into space to provide 100 terawatts of computing capacity (this entitles Musk to an additional 60 million shares)

You read that right: To access his full compensation, Musk needs to colonize Mars... and launch a fleet of satellite data centers that would equal about one-quarter of the world's data center capacity.

And that's the key to getting from our $1.3 trillion valuation to something far in excess of $1.8 trillion.

You need to believe there's a better-than-0% chance that Musk can achieve one or both of those goals in the next 10 years.

It's also important to note that, while he's entitled to a massive payday if he hits these goals, Musk already controls 85% of SpaceX's voting shares. So he's missing some of the compensation-based guardrails we usually look for in a business.

He has used his massive voting power to his advantage in the past. For example, he caught the ire of Tesla (TSLA) shareholders after he "bailed out" another one of his companies, SolarCity, by acquiring it into Tesla for $2.6 billion.

He just pulled a similar maneuver by selling xAI into SpaceX at a $250 billion valuation. And selling X (formerly Twitter) to xAI before that.

At the end of the day, Musk is a polarizing leader...

To believe in SpaceX, you need to believe in him.

This is an IPO like we've never seen before. Not only is it the largest in history... it's likely to be the most-followed among institutions and retail investors alike.

New stocks typically take up to a year to get added to index funds. But because this is such a big IPO, several index funds have changed their rules to start buying SpaceX stock as soon as its second week of trading.

That could create a lot of forced buyers for the stock.

We can't tell you where the stock will open or where it will trade in the first few months. What we can say is, from where we stand, the three businesses together are worth about $1.3 trillion... at best.

If you believe Musk will make big strides toward his extraterrestrial goals, it could be worth a lot more.

Regards,

Rob Spivey

June 10, 2026

P.S. If you missed last Thursday's urgent SpaceX briefing, you're running out of time...

The most successful analyst at our sister company, Stansberry Research, broke four years of public silence to share what he calls the "most important buy call" of his career.

He believes most investors are about to make a serious mistake with this IPO. But for a short time only, he's sharing the name of a company that could soon land on the front page of every financial news outlet in the world. Learn the details here.