For years, the private credit industry sold investors on a simple idea...

For years, the private credit industry sold investors on a simple idea...

You could earn higher yields by lending to private companies – and leave the day-to-day risks to the professionals.

Traditional banks stopped lending in the post-pandemic years thanks to soaring interest rates. Private credit looked like the future.

Industry pioneers like Blue Owl Capital (OWL) grew assets from $62 billion in the middle of 2021 to more than $300 billion. That's because it was willing to lend when banks wouldn't.

Blue Owl's early success drove massive private-equity ("PE") firms like Apollo Global Management (APO) and Ares Management (ARES) to increase their private credit exposure, too.

But all the excitement is breaking down. And while that's no secret, the situation seems to be worse than most folks realize...

Investors already had plenty to worry about...

The SaaSpocalypse rattled confidence in one of private credit's favorite sectors – software. As we covered a few weeks ago...

A good chunk of private loans went to software companies, right as AI started threatening Software as a Service business models.

And some early credit defaults raised questions about what else may be hiding beneath the surface.

Add in the conflict in Iran... and you've got yet another reason for investors to want easier access to their cash.

Bloomberg reports that this mix of fears has sparked a scramble to exit the $1.8 trillion private-credit market. Firms like Apollo, BlackRock (BLK), and Ares are facing unprecedented redemption requests.

Private credit funds aimed at wealthy individuals were built with tight redemption limits from the start. Investors can usually redeem quarterly. And most of the time, those funds only have to honor up to 5% of the fund's value in a quarter.

That structure is supposed to protect the fund from a fire sale of illiquid loans... which can have a similar effect to a bank run.

In practice, it also means investors can ask for their money... and still be told to wait...

That's exactly what is happening now.

Several major funds have already faced redemption demand far above those limits. In January, one Blue Owl fund allowed investors to withdraw about 15% of assets only after selling $1.4 billion of investments across three funds.

Other funds, like the ones mentioned above, have faced requests upwards of 10%. Some are capping withdrawals. Others are scrambling to meet requests.

BlackRock CEO Larry Fink said his firm states the 5% quarterly redemption cap right up front. But while that may be true, it doesn't make investors feel any better when they want out... and can't get out.

Private credit depends on investor confidence. The assets themselves are hard to price and harder to sell. So situations like this can become a big problem.

Once redemption requests climb past the cap, folks are forced to sit tight. That helps stabilize the portfolio in the short run... But it doesn't do much to soothe investor fear.

Nor does it help fix the portfolio.

As you can see, the situation in private credit is already bad enough...

But it might very well get worse. The software risk runs far deeper than most folks realize.

Bloomberg reviewed thousands of holdings across seven major business development companies. They're tied to firms that include Apollo, Ares, Blue Owl, and more.

The review found at least 250 investments worth more than $9 billion that weren't labeled as software exposure by one or more lenders... even though the borrowers were described that way by other lenders, PE sponsors, or the companies themselves.

Apollo classifies Kaseya, an IT management software company, as "specialty retail."

Golub Capital (GBDC) labels restaurant-management software provider Restaurant365 as "food products."

Sixth Street Specialty Lending (TSLX) considers Pricefx – which calls itself "pricing software" – to be a business-services company.

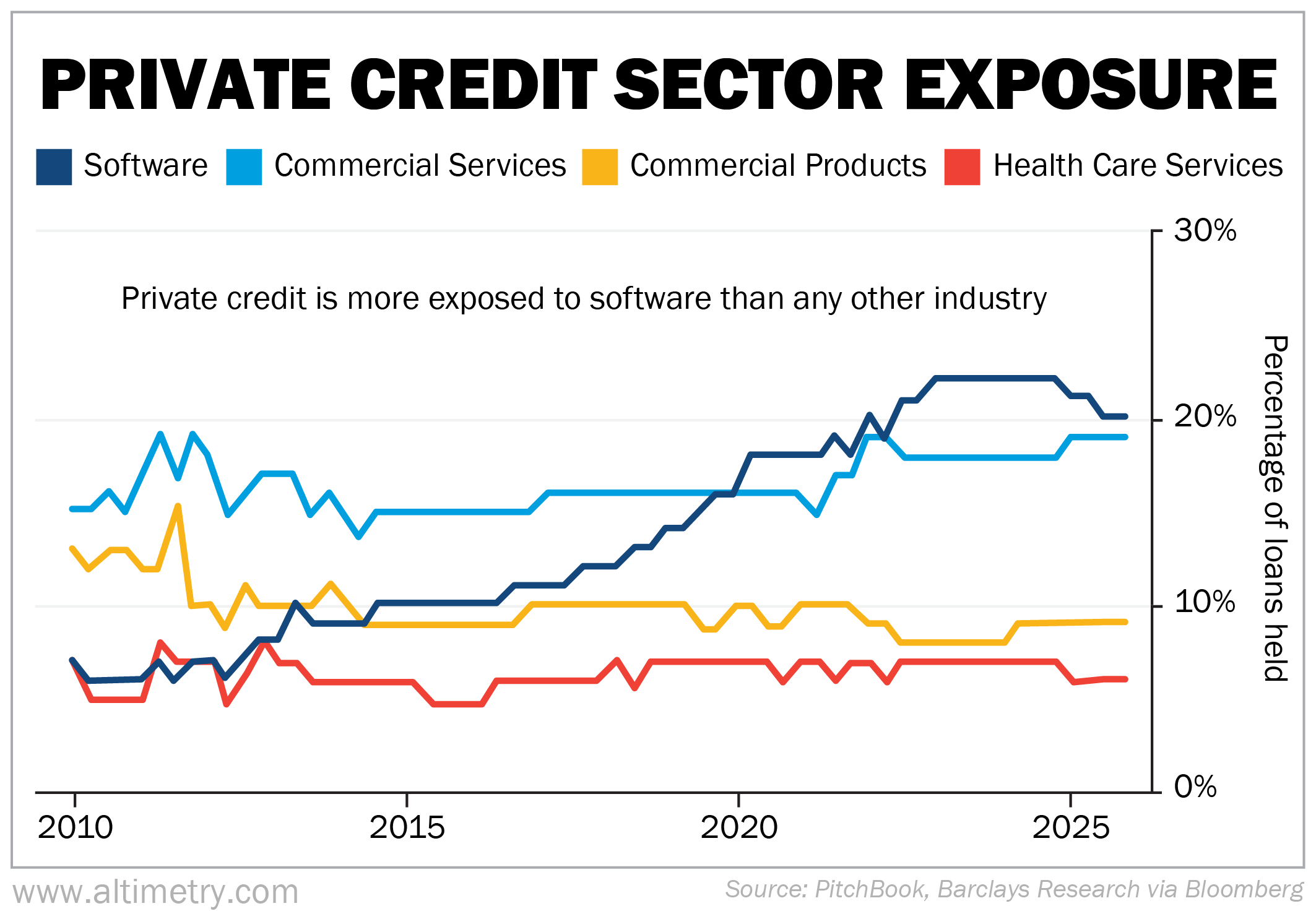

Software is already a huge piece of private credit without these mislabeled companies...

Barclays estimates the sector makes up about 20% of all loans held by private credit funds – making it the industry's biggest sector exposure.

Check it out...

You can see in the chart that private credit is already heavily exposed to software. And that's not counting the billions of dollars of debt to companies that are dubiously labeled.

In other words, the SaaSpocalypse is hitting private credit more than most folks realize. And once investors do catch on, they'll sour even more on the industry.

Investors are learning the hard truth about their investments...

Their money is harder to withdraw than they expected. And their exposure is riskier than they assumed.

That's a bad combination. It's going to keep pressure on private credit.

Firms think they can wait out the frustration by limiting withdrawals. But all that software exposure will only hurt their portfolios further. Time alone won't fix this problem.

And as for your portfolio... It's best to stay far away from this private-credit deadlock. Nothing good will come of it.

Regards,

Rob Spivey

April 6, 2026