Private creditors have always toed the line...

Private creditors have always toed the line...

They operate somewhere between traditional lending and high-risk equity.

These creditors have more room to lend – and chase returns – without strict limits. So they usually take on more risk.

Private creditors provide capital when banks aren't willing to lend... due to a business' bad credit or inadequate cash. They also offer higher returns than the bond market, which is a public asset class.

But private credit always comes with a catch. And this year, it's under heavy stress...

A good chunk of private loans went to software companies, right as AI started threatening Software as a Service business models.

Investor appetite is now cooling. And private creditors are leaning on redemption caps to safeguard cash. Now, the industry is trying to attract regular investors.

Today, we'll explain why the shift toward retail money is another warning sign that private credit is on shaky ground.

Private credit has gone from boom to bust...

This market had an incredible run from 2022 through 2024.

Higher interest rates forced struggling companies to make a choice. Either get private capital (with higher interest) or face potential bankruptcy.

That fueled a massive boom. By early 2026, the private-credit market had swelled to roughly $1.8 trillion, up from about $310 billion in 2010.

That seemed to prove its resilience. But in reality, it reflected private creditors' desperation, as they stepped into an area banks wouldn't touch.

Now, industry experts like Lloyd Blankfein are sounding the alarm...

The former Goldman Sachs (GS) CEO is calling out Wall Street for targeting everyday investors, just as...

The institutions are getting out of private-credit funds...

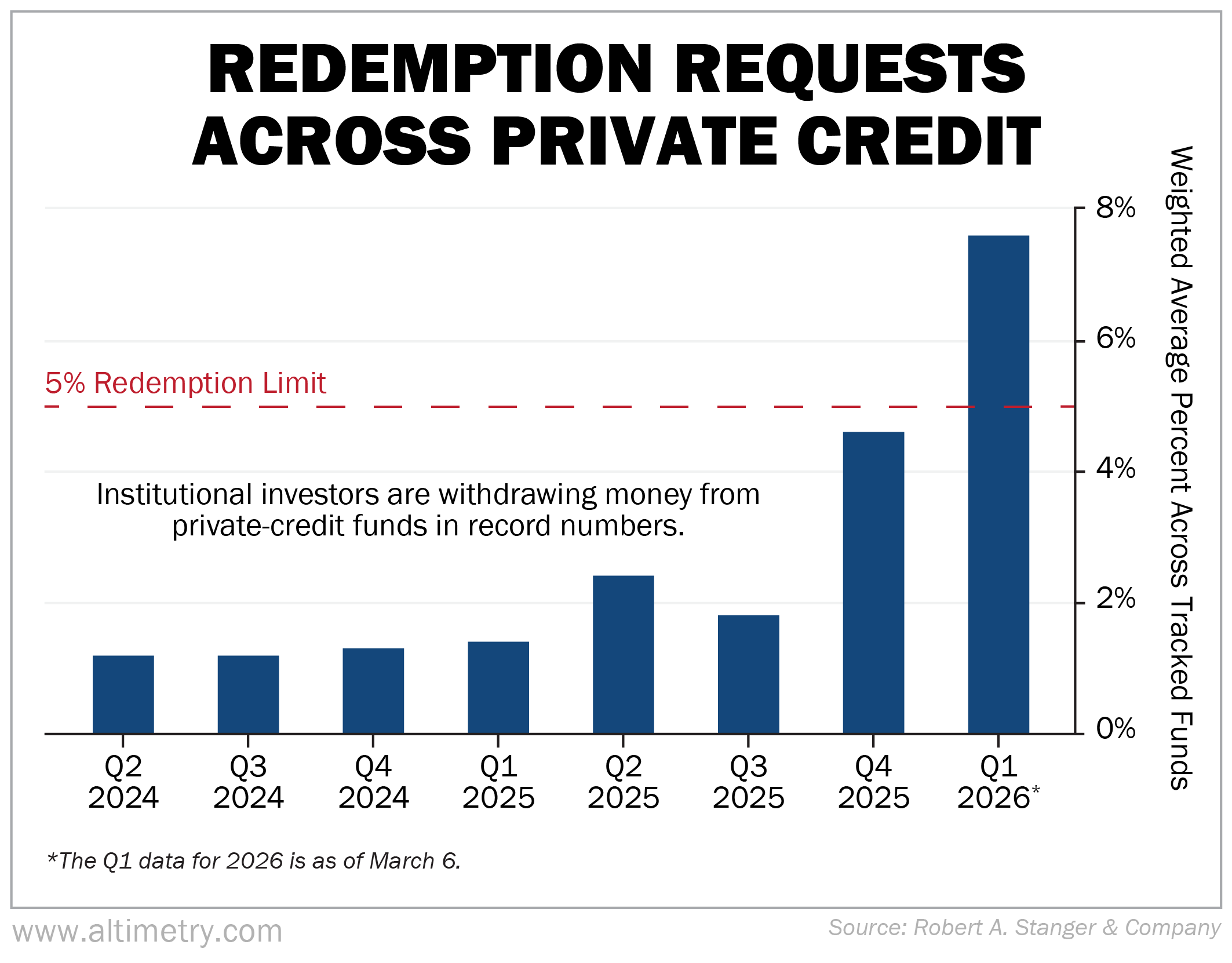

Investor redemption requests are climbing – from around 1% in 2024 to nearly 8% in the first quarter of 2026.

That's well above the 5% limit built into many of these funds. Take a look...

Keep in mind that institutional investors are withdrawing funds. They're the ones who, historically, have had access to private credit.

Private-credit managers can honor redemptions by tapping into cash and selling assets. They can also enforce caps... This would send a message that cash is more limited than many investors had hoped.

BlackRock (BLK) recently capped withdrawals from its $26 billion HPS Corporate Lending Fund at 5% after investors requested nearly double that amount. Blue Owl Capital (OWL) recently allowed investors to redeem more than 15% of net assets from a technology-focused fund... before closing the gates.

We're also seeing a spike in U.S. private-credit defaults. They climbed to 5.8% in the 12 months leading up to January 2026. That's the highest rate since August 2024.

To attract retail money, Wall Street firms are using a few tactics...

They're lowering investment thresholds and offering more liquid structures. They're also leveraging exchange-traded funds and business development companies.

But Wall Street isn't broadening access out of generosity. It needs fresh buyers...

Private credit has earned its reputation... The market is complex and often unstable. And it locks up capital for long periods.

Ultimately, private credit is best suited for institutional money.

But those investors are now heading for the exit. And as Blankfein highlighted, Wall Street is rushing to get regular people on board.

When the "smart money" needs Main Street to keep the machine running, it usually means the easy gains are gone. So retail investors should tread carefully.

Think twice before following institutions into the assets they're suddenly so eager to share.

Regards,

Rob Spivey

March 13, 2026

P.S. Right now, the stock market is in turmoil. But I can tell you exactly where, and when, to move your money... to safeguard years of hard-earned gains.

Join me live for an emergency broadcast on Tuesday, March 17. It's 100% free to join.

Don't miss this chance to get your hands on an unbeatable investment strategy – one that's outperforming stocks by 13x this year. Register for your free spot here.