The commercial real estate bloodbath has entered its final phase...

The commercial real estate bloodbath has entered its final phase...

Owners are no longer sitting on empty properties and hoping time fixes their problems... They're accepting whatever prices they can get to unload once-profitable holdings.

For example, a 485,000-square-foot office building in Chicago recently sold for $4 million. This came after changing hands for $68.1 million about a decade earlier.

The Denver Energy Center followed the same script... selling for $5.3 million after fetching $176 million in 2013.

When buildings once valued at eight and nine figures sell for scraps, the market is sending a very clear message... A huge amount of office real estate has lost its original economic purpose.

Some properties will survive lower rents and new tenants. Others are headed for conversion, demolition, or buyers with entirely different plans for building use.

That kind of reset hurts owners. But, as we'll explain, some companies are set up to profit from this office shakeout.

CBRE Group (CBRE) feeds on office turnover...

Its business covers leasing, property sales, loan origination, and property management.

Simply put, the company has its hands in every part of commercial real estate.

That means CBRE earns fees whether buildings are being leased, refinanced, revalued, or sold at a loss. It gives CBRE exposure to nearly every step in a real estate downturn.

As we mentioned earlier, the office-building market is finally moving again. For years, landlords and lenders delayed the inevitable... hoping for demand to bounce back.

But that waiting game is ending.

Distressed assets are now selling for much lower prices...

And every transaction creates fees and commissions... not to mention servicing work and appraisal assignments... for the firms that operate in the middle – the intermediaries.

CBRE is a prime example. It generates revenue through commissions and management fees tied to transactions and services.

In a market driven by forced sales, refinancing pressure, and valuation resets, that structure becomes a real advantage.

The Wall Street Journal reported that 204 distressed office buildings were purchased in 2025, up from 133 in 2024. The total deal volume was a whopping $5.2 billion.

In January and February 2026 alone, distressed office sales hit $808 million, up 24.5% from the same period the previous year.

These figures tell the story... When commercial real estate activity picks up, CBRE will benefit more than any other intermediary.

But investors seem to be missing that story...

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

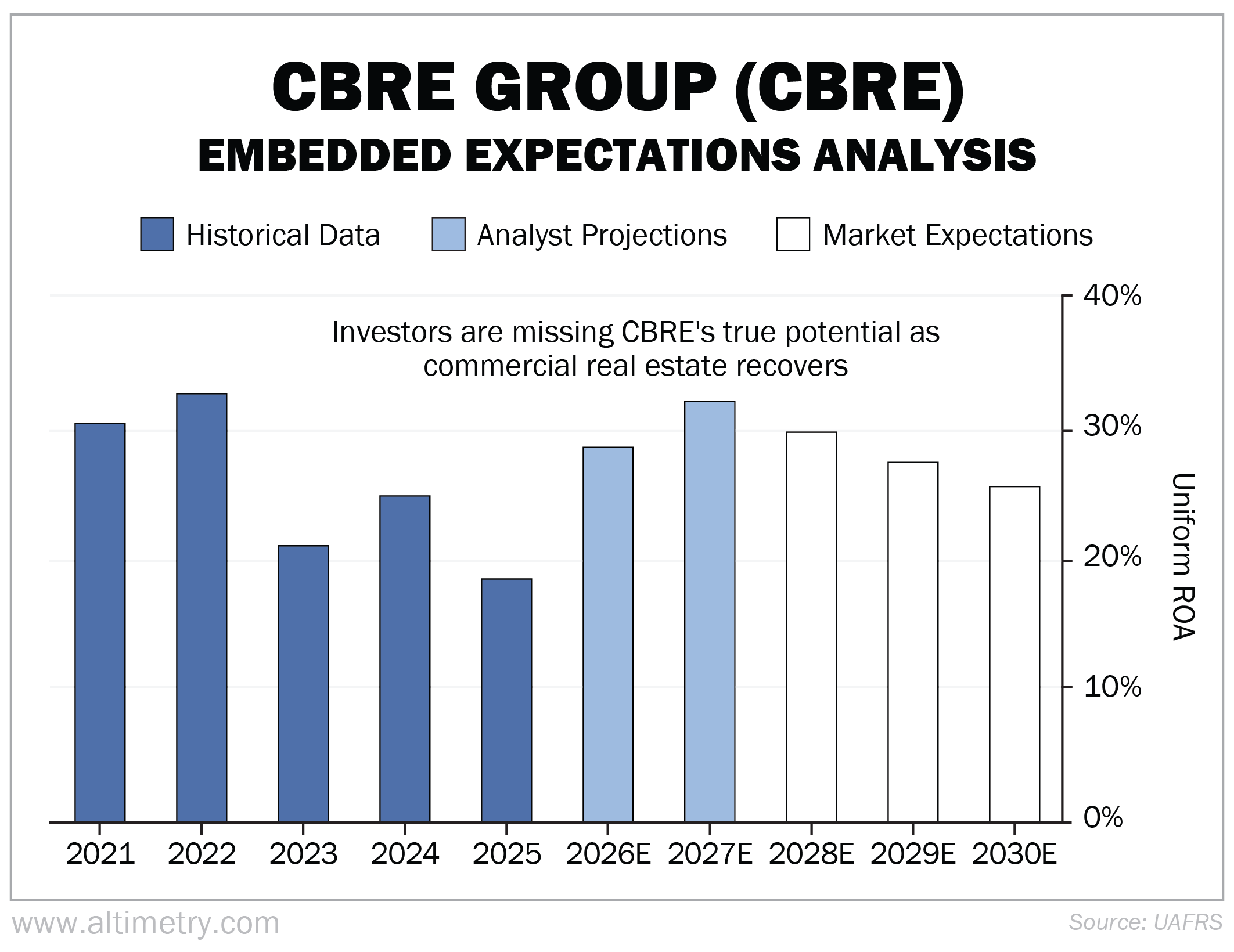

Over the past five years, CBRE's Uniform return on assets ("ROA") has ranged between 19% and 33%. Its profitability is tied to the real estate market, which was struggling. So the past few years were a bit weaker.

That said, Wall Street analysts understand that the market is recovering. Over the next two years (the light blue bars below), analysts expect CBRE's Uniform ROA to rise back to 32%. On the other hand, investors expect its Uniform ROA to only reach 26% by 2030.

Take a look...

The market doesn't think this will be a particularly strong cycle for CBRE.

But as distressed sales, loan workouts, and forced transactions pile up, that puts money right into CBRE's pocket.

The office real estate market is finally turning around...

But it's not a simple process.

Commercial landlords are still dealing with weaker demand and lower values. CBRE sits on the other side of that pain, though...

The company wins when buildings sell, no matter how high or low the price.

It also wins when loans are refinanced... and when old offices are converted into different, more profitable uses.

In sum, CBRE is emerging from a real estate bloodbath. And investors who get in now can reap the benefits... before the market catches on.

Regards,

Joel Litman

April 24, 2026