It's arguably consumers' biggest complaint right now...

Gas prices.

Need we say more?

While prices have fallen somewhat in recent weeks, they remain at record highs. The national average at the pump is $4.50 per gallon. In some states, like California, prices are as high as $5.87 per gallon.

Many folks direct their ire at the companies selling the gas – from ExxonMobil (XOM) to the mom-and-pop corner stations in their local towns.

But the truth is, these companies are paying more to buy gas, too... before it ever gets to you. To find out who's actually profiting, you have to go higher up the supply chain. The real profit is indicated by something called the "crack spread."

The crack spread is a measure of the value of refining. Refiners extract crude oil from the ground. This crude oil is then separated and turned into the gas and diesel that get pumped into everyone's vehicles. The spread comes from the price difference between the raw oil and the finished products.

Typically, different companies take part in each level of this process. A refiner extracts the crude product and refines it. Then, it sells that finished product to a gas station. The end result is what powers your car or truck.

This is why distributors (like gas stations) don't actually profit much from higher gas prices. They're forced to buy refined gas at a high price. And they can't raise their own prices a lot to compensate. If they did, consumers would go to cheaper stations down the road.

Today, not only are gas prices high, but the crack spread is large as well. The crude product is selling for cheap, while the refined product is expensive.

This means the companies that refine gasoline are the ones turning the biggest profits. And those that do it all are benefiting the most... like Shell (SHEL).

Shell is one of the few vertically integrated companies in the gas industry. The company does it all – extraction, refining, and distribution.

Shell benefits from the high crack spread. It can cheaply extract oil while selling it at extremely high prices as gas.

At first glance, it looks like the market has caught on to Shell's potential...

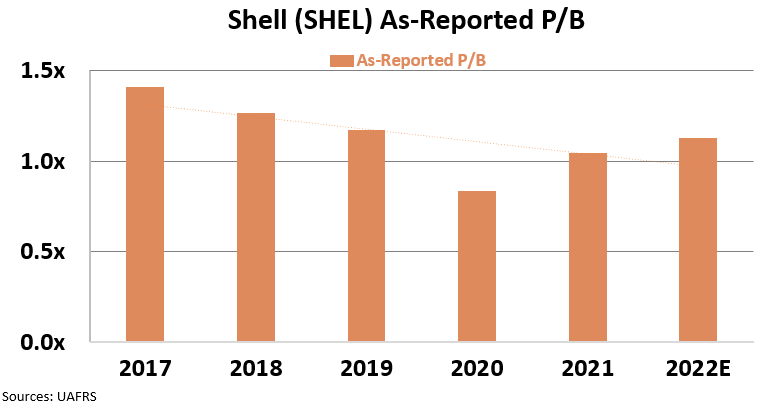

The high crack spread means Shell is set up to profit. However, to understand how the market feels about the company, we have to turn to the price-to-book (P/B) ratio.

The P/B ratio helps us understand how the market values Shell's assets. That includes all of the oil, drilling rigs, and gas stations it owns.

At a 1 times P/B ratio, the market values a company's assets at book value. If the ratio is lower, investors are discounting the company. If it's higher, it's trading at a premium.

Shell has had an as-reported P/B of more than 1 times since 2017, excluding a dip in 2020. This means the market is willing to pay more for Shell stock than its assets are worth.

The market seems to understand that high crack spreads will mean premium profitability for Shell in the future.

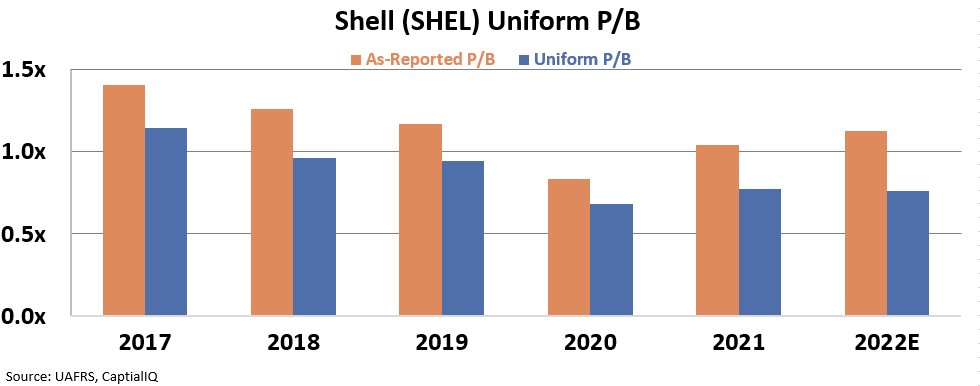

However, the real P/B ratio flips this story on its head...

When we use Uniform Accounting to clean up the financials, we see that Shell isn't trading at a premium, after all. Its Uniform P/B ratio is 0.8 times, which means the market isn't even willing to pay the value of the company's assets.

You'd typically see a 20% discount like this if the company had poor returns, bad management, or was undergoing a profitability crisis.

But this discount comes during a record-strong oil market. The market is just being blinded by the inflated as-reported P/B ratio.

Based on the oil market's resilience, Shell is positioned for a strong outlook as prices at the pump continue to soar.

It's arguably consumers' biggest complaint right now...

It's arguably consumers' biggest complaint right now...