Americans are breaking out their credit cards for the holiday shopping season...

Americans are breaking out their credit cards for the holiday shopping season...

It's no shocker that around 70% of the U.S. economy's output is powered by consumer spending every year. Americans simply love to shop.

During the holidays, consumer spending reaches its peak when gift-givers splurge on fancy gadgets and trendy apparel.

This year, the National Retail Federation forecasts that the average U.S. consumer will spend nearly $1,000 on holiday shopping.

Some consumers wary about debt and interest charges might look to avoid putting these purchases on their credit cards.

These days, credit-skeptical consumers are becoming fewer and fewer.

The reality is that a greater share of spending will end up on credit cards in the future as the digital-payments revolution gathers momentum.

This is especially true as the pandemic pushes more retail purchases online and companies like Walmart (WMT) and Target (TGT) increase their e-commerce presence.

Going forward, expect more Americans to have physical and digital wallets...

One household name is a major winner of the digital-payments revolution...

A major beneficiary of the surging growth in digital credit card payments is Visa (V).

The payment processer is among the largest of its peers by market capitalization and is one of the companies that arguably created the industry.

With its dominant position alongside Mastercard (MA) in a duopolistic market, one would expect Visa to generate outstanding profitability.

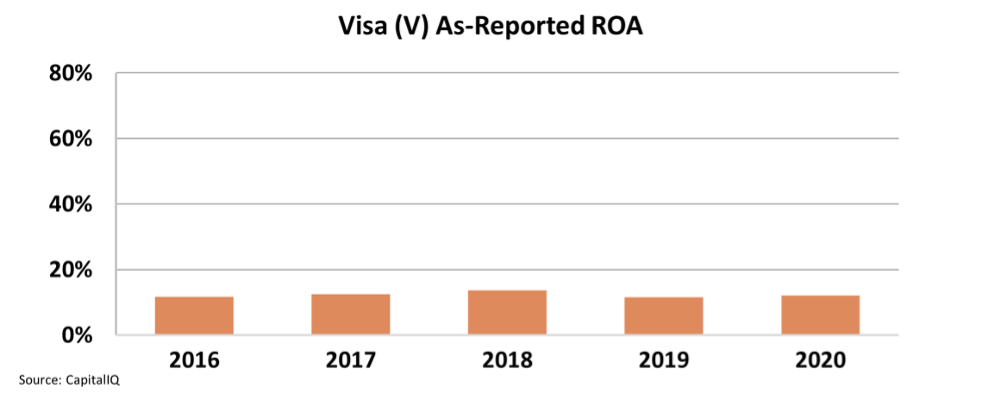

But it looks like the company is a run-of-the-mill U.S. corporate giant based on an as-reported basis. Over the past five years, its as-reported return on assets ("ROA") has been trundling along between 12% and 14%.

For context, the average corporate ROA in the U.S. is 12%. This means as-reported metrics tell us Visa is an average company.

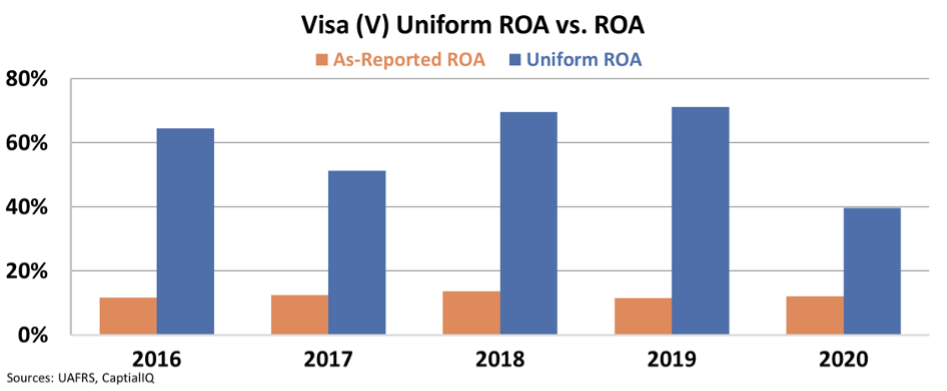

In reality, investors understand that Visa is no average company. The reason why is clear once you account for the distortions inherent to as-reported metrics.

Using Uniform Accounting, we can see that growth in credit card usage has massively bolstered Visa's profitability.

Putting aside the pandemic year in 2020, the company's Uniform ROA over the past half-decade has consistently been above 50%.

With returns almost 5 times greater than corporate averages, Visa has seen tremendous success as more and more Americans turned to credit cards for e-payments in the past decade.

The digital transformation and further adoption of digital payments will only accelerate this trend in the future.

Finding the next Visa before it's a megacap...

Visa's success has led to massive wealth creation for the company's investors.

Since its initial public offering ("IPO") in 2008, early public investors have seen 12 times returns as the stock price has soared.

While still impressive, the reality is that public investors have missed most of the biggest move higher for Visa.

The reason is that the company's IPO was 50 years after it was originally created.

Visa started inside Bank of America (BAC) and a broader consortium of other banks several decades ago.

By the time it reached the New York Stock Exchange as the largest IPO of its time, it was already valued at $18 billion.

Visa's timing for going public was great for the company but ill-timed for public investors. They have had to settle with 12 times returns.

Sometimes, promising tiny companies that go public with less than $1 billion in value can yield higher returns.

Here at Altimetry, when we are stock-picking, we're searching for that undiscovered diamond in the rough...

We are looking for the kind of return public investors got from companies like Equinix (EQIX), which went from a $10 million company in 2003 to being worth more than $70 billion today.

That's roughly a 5,300 times return. Every $1,000 invested in EQIX in 2003 is worth more than $5 million today.

So, let's put that into perspective. Visa would need to be worth $100 trillion today to have produced a similar level of return...

The unfeasibility of massive returns from these large-cap names is why we spend so much time hunting for microcaps...

We want to help readers subscribed to our Microcap Confidential service find potential opportunities for transformative wealth creation... finding names like Equinix that can turn $1,000 into millions.

That's why tomorrow at 8:00 p.m. Eastern time, we're holding a special event to highlight our favorite microcap stocks.

At our special investment summit, we'll tell you why we are so bullish for 2022 and name a few stocks that are poised for a banner year.

Make sure to join us by registering for free right here. It's something you don't want to miss.

Regards,

Rob Spivey

December 15, 2021