Editor's note: The markets and our offices are closed on Friday, July 3 for the Independence Day holiday. Because of this, we won't publish Altimetry Daily Authority. Please look for your next edition on Monday, July 6.

On behalf of the Altimetry team, we wish you a safe and relaxing holiday weekend.

Qualcomm (QCOM) spent years trying to convince investors that it could do more than power smartphones...

Qualcomm (QCOM) spent years trying to convince investors that it could do more than power smartphones...

The company dominated the chip market for those devices. Then it expanded into cars, connected devices, and PCs.

This was right around the time investor attention shifted to AI. But Qualcomm couldn't keep up.

Its revenue peaked at $44 billion in fiscal year 2022 and then slipped to $36 billion during the handset downturn. (Global smartphone shipments and sales fell about 4% in 2023.)

The business survived the slump, recovering to $44.3 billion in fiscal year 2025. But it has been treading water since then.

Today, we'll look at how Qualcomm is finally entering the AI market, and why investors have yet to price in a return to stronger profitability.

Qualcomm's data-center push is no longer a side project...

Smartphones run on a tight power supply, so their batteries need to last. Data centers now face a similar constraint... at a much larger scale.

At its June 24 Investor Day, Qualcomm unveiled its infrastructure roadmap for the AI and data-center markets. This included the Dragonfly C1000 data-center CPU and other new products.

Its data-center lineup aims to maximize performance per watt and lower total costs over the life of chips.

According to Qualcomm, Meta Platforms (META) agreed to use the Dragonfly C1000, and future iterations of the CPU, in its AI infrastructure starting in 2028.

AI power demand keeps growing. Yet power availability is becoming one of the biggest bottlenecks for hyperscale operators.

Qualcomm is trying to bring its "wireless DNA" into that environment.

Its data-center expansion should produce billions of dollars in revenue starting next year...

Qualcomm lifted its fiscal 2029 non-handset revenue target to $40 billion, roughly twice its prior goal. At least $15 billion is expected to come from data centers.

That's a major shift for a company that investors still associate with cell phones.

And that seems to be what the market is worried about... Wall Street analysts expect Qualcomm's smartphone revenue to fall between $5 billion and $6 billion heading into next year.

This is exactly why the data-center pivot matters.

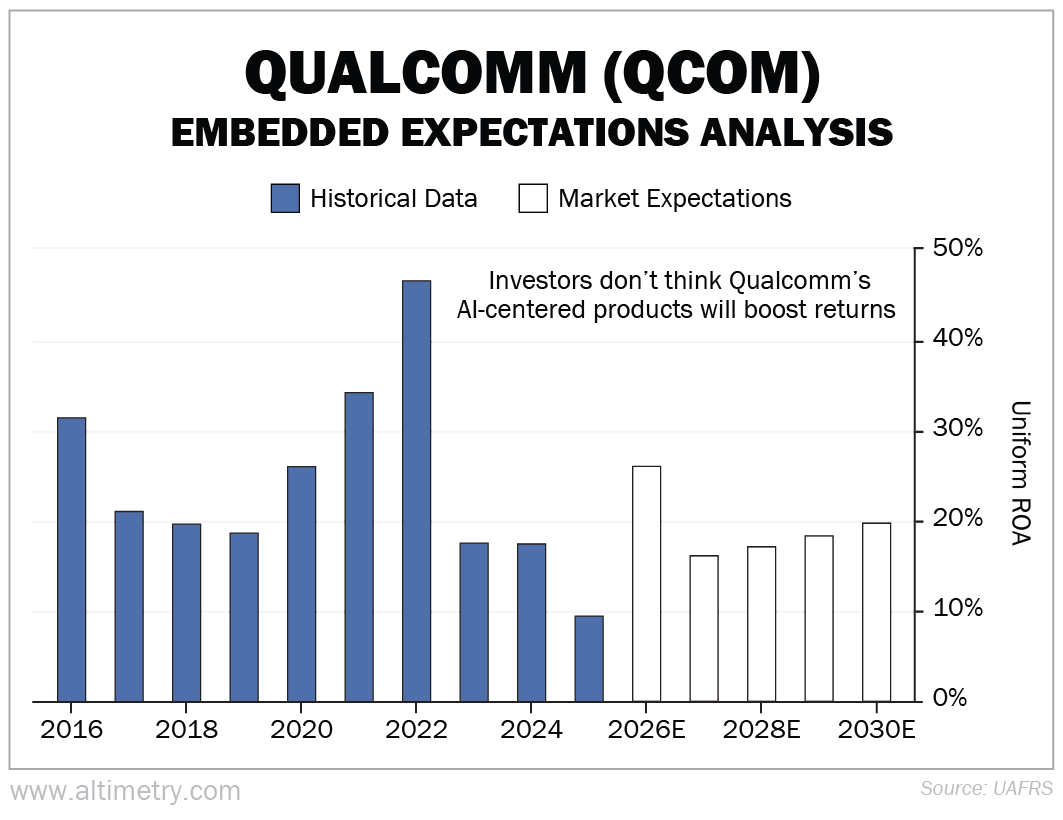

Despite record demand, investors aren't optimistic about Qualcomm's long-term performance...

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Over the past decade, Qualcomm's Uniform return on assets ("ROA") was consistently above 20%. That means the company generated big profits through its core chip franchises.

When the handset downturn hit, the company's revenue fell and investor confidence collapsed. After three rough years, the market appears to be treating the 20% Uniform ROA as a hard cap, even though Qualcomm has spent years performing above that level.

Take a look...

The market expects the post-2022 version of Qualcomm to persist, even as the company's revenue mix shifts toward a much bigger AI opportunity.

Qualcomm missed the first wave of the AI trade, but it can still win...

Qualcomm's AI business is young... Its data-center products are only beginning to ramp up.

That said, the company now has a major hyperscale customer in Meta... And it's inking agreements for a brand-new chip line.

Management has nearly doubled its revenue expectations for non-smartphone chips by 2029. That tells us the company's growth will be stronger than investors currently expect.

They've spent years learning to discount Qualcomm.

But now, it's reverting to the profitability investors used to see... while staking its claim in an entirely new market.

Regards,

Joel Litman

July 2, 2026