Ben & Jerry's is turning up the heat on Unilever (UL)...

The popular ice-cream brand is taking its owner to court. But the most surprising part of this story is why... You see, Ben & Jerry's wants Unilever to stop some sales of its products.

Specifically, the company's independent board is protesting Unilever's recent deal to sell its products in the Israeli-occupied West Bank region. The ice-cream company claims this goes against its core values.

As you can imagine, the lawsuit is causing a great deal of friction.

Ben & Jerry's has a long history of putting environmental, social, and governance ("ESG") values at the forefront of its operations. It has made special flavors in support of various movements, like Change is Brewing to support racial justice... and Americone Dream in partnership with Stephen Colbert's charity fund.

In July 2021, Ben & Jerry's announced that it would end sales in the West Bank and parts of East Jerusalem following pressure from pro-Palestinian activists. But recently, Unilever agreed to sell the company's Israeli operations to a local distributor. That's why the ice-cream company decided to sue.

Unilever has known about its subsidiary's stance toward the West Bank for some time. So it's odd that it waited until now to go against its wishes.

It seems like ESG is taking a backseat for Unilever...

Historically, Unilever has been at the forefront of all things ESG. The company strives to reduce its environmental impact across its brands. And it has a strong track record of prioritizing ethics in business practices.

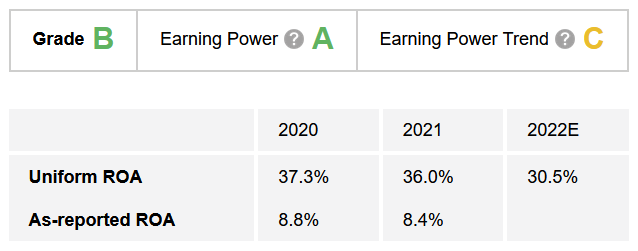

Uniform Accounting shows that this approach has benefited the company in the past.

Our Altimeter tool gives us easily digestible grades to rank stocks based on their real financials. It does this by eliminating the distortions in generally accepted accounting principles ("GAAP") financial metrics.

As-reported metrics paint Unilever as a modest company. Its return on assets ("ROA") was 9% in 2020, below the corporate average of 12%. Last year, ROA declined to 8%.

These numbers aren't impressive. And they don't suggest that prioritizing ESG has done much for the company.

But Uniform Accounting shows otherwise... Unilever's Uniform ROA was 37% in 2020. And it stayed at a healthy 36% in 2021. That's why Unilever earns an "A" Earning Power rating.

But the Altimeter also shows that ROA is expected to fall off this year, giving the company just a "C" for Earning Power Trend.

It looks like being an ESG leader isn't benefiting Unilever like it has in the past. Now, management is scrambling for a new strategy.

This could explain the company's decision to ignore Ben & Jerry's and sell its products in the West Bank. Perhaps it decided that standing by its ESG narrative is less important than maintaining relationships with Israel and earning a few extra dollars.

Let's see what the market thinks of this shift...

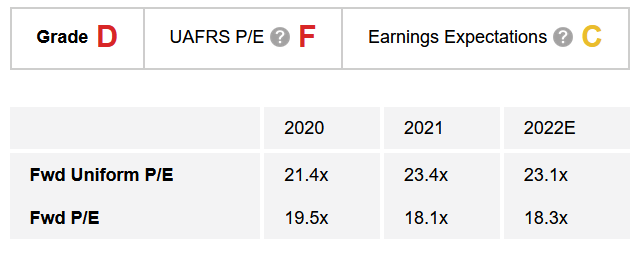

In order to determine whether Unilever is a good buy, we must consider valuations in addition to fundamentals.

Uniform Accounting shows that the company is even more expensive than it appears. Unilever's P/E ratio was 21 times in 2020 and 23 times in 2021. That number is expected to remain at 23 times in 2022.

The market is paying a premium for Unilever, even as returns start to decline in the face of a possible ESG strategy shift. Investors should be wary. This new strategy could lead to higher sales... or drive ESG-focused customers away from the brand.

AI-driven electricity demand is creating a durable tailwind for natural gas infrastructure. And one company is better positioned than the market expects...

Ben & Jerry's is turning up the heat on Unilever (UL)...

Ben & Jerry's is turning up the heat on Unilever (UL)...