Software as a Service ('SaaS') businesses used to be the gold standard for tech investors...

Software as a Service ('SaaS') businesses used to be the gold standard for tech investors...

These companies don't have many tangible assets. So they keep costs low... and profit margins high.

They also charge fees for their SaaS platforms, which generate stable, predictable revenues. That was the norm for about 15 years.

Once AI came along, things changed. This new technology has recently threatened to make software companies obsolete.

The "SaaSpocalypse" hammered even the biggest software stocks. And investors have started looking for safer havens.

We're now seeing a shift toward capital-intensive businesses. Goldman Sachs calls it the "HALO" effect – short for companies with "heavy assets and low obsolescence."

And they're gaining momentum. After all, AI can write code... but it can't build an aircraft or a car.

But there's more behind the recent market shift. Today, we'll explain why investors shouldn't make decisions based on asset type alone.

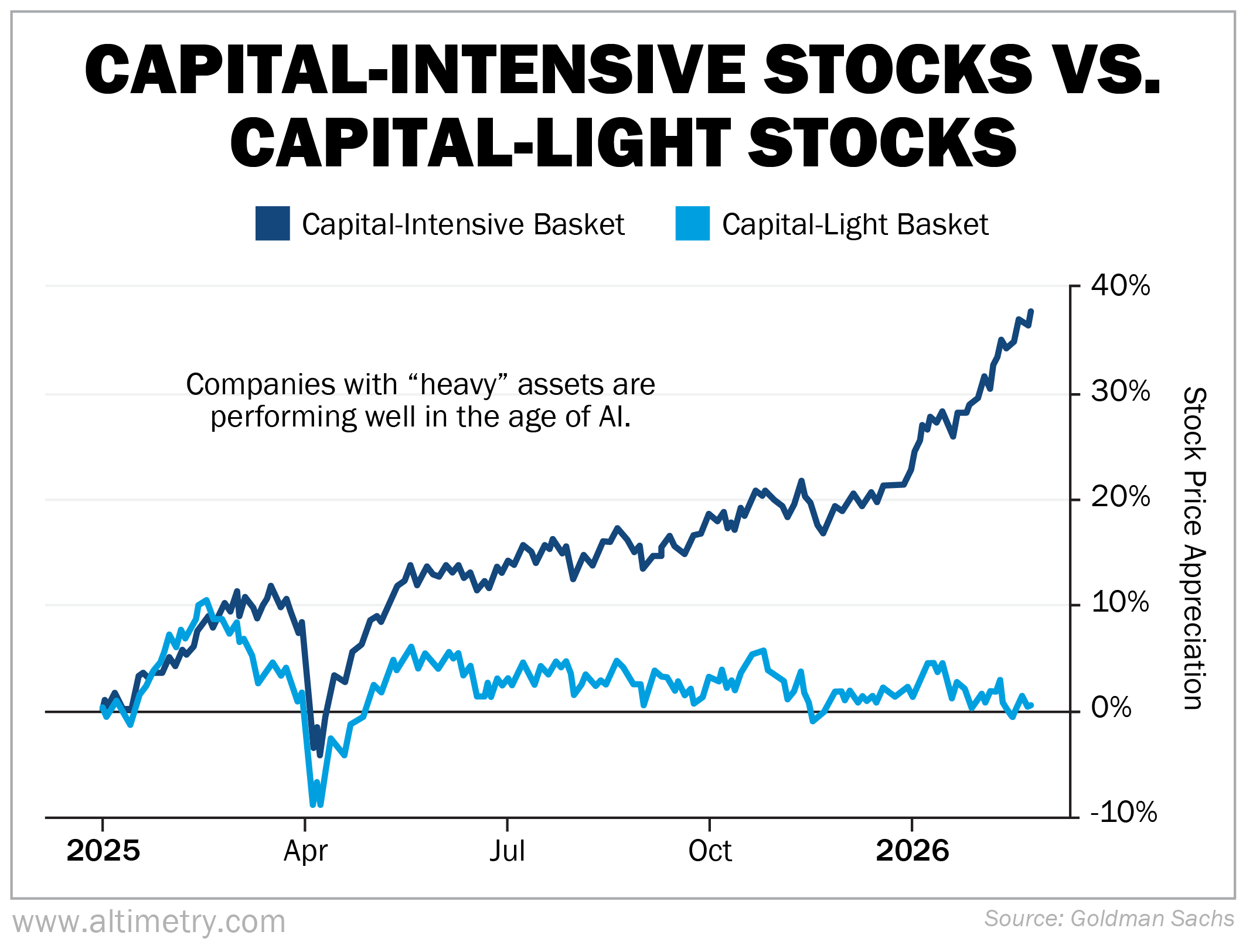

To understand the HALO effect, Goldman Sachs has divided stocks into two 'baskets'...

The "capital intensive" basket includes manufacturers... like semiconductor equipment maker ASML (ASML), industrial gas supplier Air Liquide (AIQUY), and aircraft giant Airbus (EADSY). These stocks are up 100%, 24%, and 22%, respectively, since the start of 2025. These are the HALO trades.

The "capital light" basket includes digital firms... like payments giant Adyen (ADYEY), shipping and logistics company DSV (DSDVY), and medical imaging specialist Siemens Healthineers (SEMHF). They're down 29%, up 19%, and down 17%, respectively.

The capital-intensive batch has outperformed the capital-light group by about 35% since the start of 2025. Take a look...

The U.S. market seems to be favoring hard assets... and moving away from businesses built on digital or human capital.

But the reality of investing is much more nuanced...

Take ASML. Yes, it's an asset-heavy business. It builds some of the most advanced semiconductor manufacturing equipment in the world.

But investors aren't rewarding ASML because it owns a lot of equipment. They're moving into the stock because it sits at the center of the AI infrastructure build-out.

Chipmakers can't build chips without ASML's equipment. In fact, the more advanced the chips, the more companies need ASML's top-of-the-line etching systems. (These tools print the tiny patterns you see on microchips.)

Airbus has a similar story. Aircraft manufacturing is one of the most capital-intensive businesses in Europe. Airbus also benefits from the region's renewed defense push. Last year, the company's defense segment trounced its commercial aircraft segment... growing 11% versus just 4%.

On the flip side, Adyen was one of the biggest losers in the asset-light basket. But the international payment processor wasn't hurt because of its asset type.

Ayden works with large Chinese merchants that sell products in the U.S. And last April, the tariff news rocked the business. U.S. website traffic to the online marketplace Temu, for example, dropped by 52% between March and May 2025.

There are countless more examples. And resilience is the key to their success...

We know that AI models can develop software. But it can never replicate the decades of customer data companies – like Intuit (INTU) – use to train those models. It's a one-of-a-kind asset-light business.

When a company like U.S. automaker Ford (F) pivots into AI data-center battery storage, that doesn't mean that segment will skyrocket just because it's asset-heavy. It has to prove its muscle in that new business line.

The point is, a factory isn't valuable simply because of its equipment. And a digital business isn't inherently replaceable. What matters is what a company does with its assets – and whether it can thrive in the age of AI.

So don't spend too much time sorting companies into different buckets. And certainly don't get carried away with HALO trades. Focus on assets that are proving to be indispensable in today's market.

Regards,

Joel Litman

March 19, 2026