Everyone has a favorite way to fly...

Everyone has a favorite way to fly...

You may favor low-cost carriers that offer cheap flights with fewer amenities. Or maybe you prefer full-service airlines and free checked bags.

At the same time, almost everyone has a horror story about flying. Delays, bad customer service, or shrinking legroom can ruin an airline's reputation.

I'm sure that at least one air carrier popped into your head while reading that. And many of these airlines have one thing in common...

Your local airport is its hub, so you're stuck with it. That likely either makes you thrilled or furious.

Both your favorite and your least favorite airline have another shared characteristic that you probably haven't considered. And if you've ever thought about investing in these companies, it's an important one.

Today, I'll talk about an overlooked revenue stream that can make or break airlines... and what it means for one airline in particular.

As I'll show, investors could be missing a big opportunity because they're focusing on the wrong data.

Flights have almost nothing to do with how much airlines are worth...

When investing in airline stocks, you'd normally pay attention to factors like flight volume or average revenue per seat. The prevailing logic is that these data points tell you a lot about an airline.

However, folks often ignore an entirely different metric. When valuing your favorite airlines as an investor, the service of their actual flights isn't all that important.

What really makes a difference are their frequent-flyer programs.

Frequent-flyer programs let you generate points on your preferred airlines. Most airlines have programs that offer "miles" based on how much you travel in a given year. Some even let you generate miles when you make purchases on a branded credit card.

Said another way, you get rewarded for loyalty. And so does the airline.

Delta Air Lines (DAL) is a great example of this. The company's market cap is about $25 billion. Its SkyMiles rewards program is worth a staggering $28 billion.

Delta has hubs in a bunch of big cities, like Atlanta, New York, Los Angeles, and Seattle. That means a lot of potential loyalty customers.

When a savvy investor is considering putting his money in Delta, there's more to look at than just flight revenue. Delta's financials are totally different when you factor in its loyalty program. It makes the business much more profitable.

Airlines are notoriously tricky. Planes are expensive to buy and maintain. All kinds of delays and issues are outside of these companies' control. Fuel and labor prices eat away at their margins.

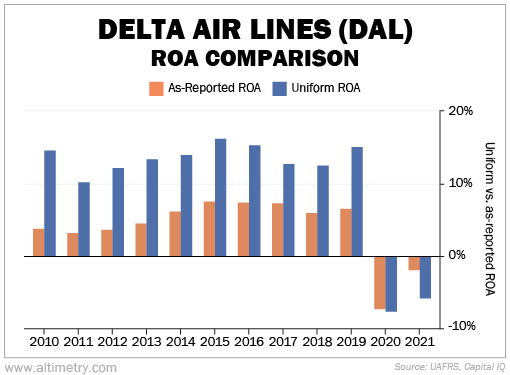

That's why airlines have a history of losing money. Even Delta has weak returns on an as-reported basis.

Over the past decade, the company's as-reported return on assets ("ROA") peaked at about 7%. It averaged 4%... and the company's cost of capital is around 6%.

In other words, Delta looks like it's losing money in the long run.

Here's the problem... This doesn't factor in the value of Delta's loyalty program.

These programs help keep airlines alive.

As you earn miles, you're effectively paying the airline ahead of time. This keeps airline companies from losing all their money during rough times.

In Delta's case, people will often exchange their points for SkyMiles on regular credit cards to plan for future trips. There's no reason not to... It's "free" to make this exchange from a regular consumer point of view.

However, these payments don't always show up in the right places on company financial statements. Companies can only book revenues when the service is provided. (That's called the "matching principle.")

Rewards revenue normally gets offset by an "unearned revenue liability," which makes the business look worse than it is. To counteract this, Uniform Accounting shows the revenue coming in when the company actually gets it.

Take a look at the following chart. It shows Delta's Uniform financials – adjusted for the full value of its loyalty program – versus its as-reported ROA.

We can see that it's actually a profitable airline in normal times. Its Uniform ROA peaked around 16% in 2015.

Check it out...

Delta's loyalty program alone couldn't keep it profitable during the pandemic. Its Uniform ROA flipped negative in 2020 and 2021. And as-reported ROA looked far better in 2021 due to a $4.5 billion government grant, which we don't include under Uniform Accounting.

However, the past decade of returns makes our point... Investors simply don't realize how much of a buffer the loyalty program provides. The as-reported numbers certainly don't show it.

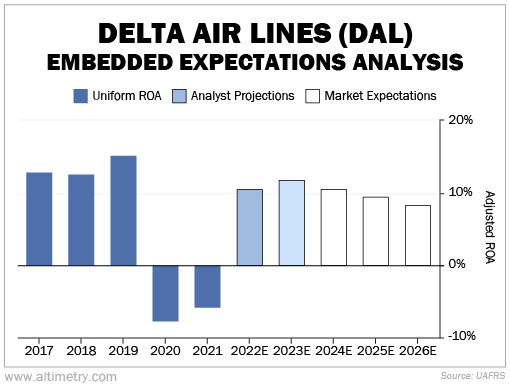

And investors expect Delta's performance to be much weaker than the historical average from here.

We can see this through our Embedded Expectations Analysis ("EEA"). It uses Uniform Accounting to show us what investors expect from a company based on its current stock price.

The market expects Delta's long-term Uniform ROA to settle at around 8% by 2026. That's way below its normal performance.

Take a look...

Investors expect a rough post-pandemic recovery for airline companies. These folks either don't understand how valuable Delta's loyalty program is... or they think it's going to become weaker in the future.

That means – if you believe nothing has changed about the company – Delta is trading at a discount to the value of its loyalty program.

Delta has the largest loyalty program in the world...

That's unlikely to change in the near future. Even if its flights don't recover soon, it could still survive on its loyalty program alone.

Since 2020, the SkyMiles program has risen by $2.5 billion in value... about 10% of the company's market cap. That's a good revenue stream to supplement the business.

We wrote about the opportunity in Delta back in early October. Since then, the stock is up 24%. And there's plenty of room for growth from here...

Shares are still down more than 30% from pre-pandemic levels. Investors should eventually come back around to the value of Delta's loyalty program. That could lift Delta's valuations before flight activity fully recovers.

Regards,

Joel Litman

February 14, 2023