Nobody wants to hear that gross domestic product ('GDP') is shrinking...

Nobody wants to hear that gross domestic product ('GDP') is shrinking...

Normally, the statement "the economy contracted this quarter" generates a lot of buzz, including several days of headlines and a pullback in the stock market.

There is a symbolic danger to a contraction beyond the headline shock, as it means the economy is only a quarter away from a potential recession. And when a recession strikes, the worries often last longer than a single quarter.

GDP shrinkage usually points to structural issues in the economy. These issues could lead to trouble in the stock market, and they could even potentially indicate a prolonged recession like the one we saw in 2008.

With recent recessions still fresh in investors' minds, you'd expect the announcement that the U.S. economy is shrinking to lead to some volatility and a major round of headlines.

Surprisingly, instead of the usual buzz, most people shrugged it off when it was announced that GDP shrank by 0.4% last quarter.

Even though the first quarter was tough, the economy is in a prime position to grow...

You might see some folks talking about how the economy is on the verge of an imminent collapse, but the underlying data paint a vastly different picture.

Consumers continue to demonstrate confidence in the shape of the economy by putting their money to work. Just last week, we highlighted how consumer balance sheets remain strong.

These balance sheets are a crucial measure of the health of the overall economy, since so much of the U.S. economy is driven by consumer spending.

The headwinds the market has experienced have little to do with consumer spending levels, which is part of why the market didn't fall on the GDP contraction announcement. Rather, declining inventory levels can be traced back to inflation and supply chain woes.

After a quarter of inventory buildup at the end of 2021 due to supply chain issues and the war against Ukraine, U.S. consumers and corporations want to buy more than is available. This desire paired with the inability to spend is the root of the GDP contraction.

We're still so confident in the market today because the underlying credit picture remains pristine, and further infrastructure spending will send earnings higher. When consumers and corporations buy from each other, it creates a virtuous cycle where everyone comes out richer.

Meanwhile, unlike the inflationary spiral seen in Weimar Germany or Zimbabwe in 2009, inflation in the U.S. has not been nearly as destructive.

Instead, current inflation is due to supply chains reaching the end of their life cycles combined with pent-up demand.

This means that as supply chains right themselves, spending will return to normal and GDP can grow.

Taken together, this all signals long-term strength.

For more evidence of this, we can see that management teams are getting more bullish about the market, even as stock prices are falling.

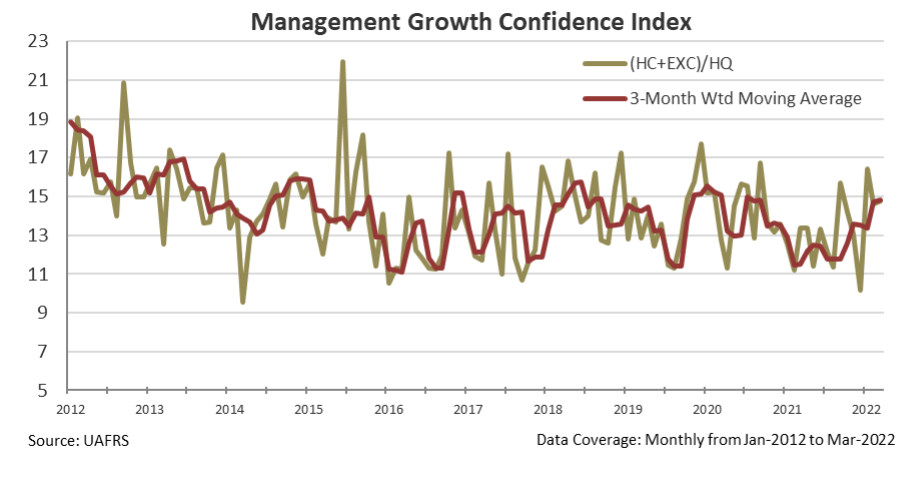

Just as we can quantify the degree to which growth is already priced into companies' valuations, we can also quantify aggregate management confidence levels.

Our Management Growth Confidence Index is based on our Earnings Call Forensics ("ECF") work. ECF is our proprietary auditory analysis tool that uses changes of cadence, pitch, and other vocal qualities during earnings calls to identify when management is excited, highly confident, or highly questionable about a topic.

We can sense management teams' confidence levels by looking at the ratio of excitement and confidence markers to questionable markers.

While we typically use this as an additional signal in our stock-picking process, we can also use it as a macro signal by aggregating recent calls across the entire market.

When the Management Growth Confidence Index is high, it generally means that management teams are more bullish on their short- and medium-term outlooks.

As you can see below, the red line, or three-month moving average, has been trending up to where it was in late 2020. Back then, leadership teams saw many opportunities to invest as society emerged from the pandemic, which drove stock prices higher in 2021.

Today, they are seeing the same opportunity to invest...

And just as was the case back then, sentiments are high once again.

Spending across the spectrum is growing, including for corporations. As management is confident for the future and is therefore willing to open the purse strings, the economy will pull out of the current doldrums on the back of renewed corporate spending.

Regards,

Joel Litman

May 23, 2022