Our power grid is being taxed more than ever before...

Our power grid is being taxed more than ever before...

And it's not just electronics anymore, although they're contributing plenty of stress. All those gadgets are constantly sending and receiving data. The data centers that feed them use massive amounts of energy all day.

It's also the millions of electric vehicles ("EVs") we're plugging in every night... and billions of dollars' worth of home solar panels. The average U.S. citizen is using more electricity than ever.

And the legacy power grid is struggling to handle it all.

According to Bloomberg, dangerous power quality is putting at least a million U.S. homes at risk. From 2015 to 2019, fire departments responded to an average of 46,700 home fires per year due to electrical failures.

Overloads are taxing U.S. utility infrastructure. The wiring of many older houses and other buildings simply can't handle unexpected surges.

All that infrastructure is going to need an overhaul... and power-infrastructure companies will be some of the top beneficiaries. Today, we'll look at one thriving business that could be even stronger than the market thinks.

Quanta Services (PWR) is at the center of a new power-infrastructure investment cycle...

Quanta is one of the largest construction and engineering (C&E) companies working on the U.S. power grid. And business has been booming for the past few years... Revenue surged from $11 billion in 2020 to an all-time high of $21 billion in 2023.

Last November, the Biden administration announced another $3.9 billion in funding to modernize and expand the U.S. power grid. A lot of that cash could end up in Quanta's pockets.

Shares of Quanta are up more than 50% in the past year. So investors understand that the company is doing well.

And yet, they don't seem to get just how much the company benefits from all this infrastructure spending.

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA works a lot like a betting line in a sports bet. We use Quanta's current share price to calculate what investors expect from future performance... and compare those forecasts with our own.

It tells us how well our "team" (the company) has to perform to justify the market's "bet" (the current price).

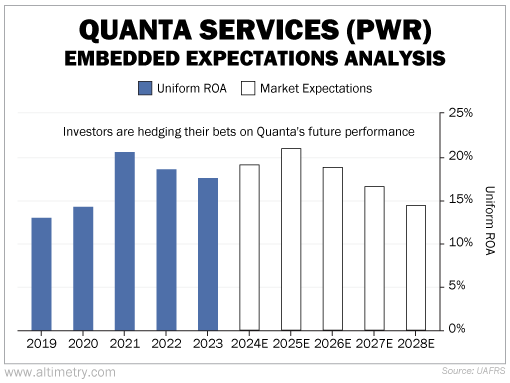

Prior to 2021, Quanta was an OK business. Its Uniform return on assets ("ROA") averaged about 12%, which is also the U.S. corporate average.

In the past three years, Uniform ROA surged closer to an average of 19%. And the market is pricing it to fade back to 14% by 2028.

Take a look...

Investors can't seem to decide if Quanta will keep up its recent streak... or if it will fall back down to average. While they don't expect Uniform ROA to stay as high as it was, they also don't expect it to plunge.

But the U.S. needs to invest in our power grid to keep it running safely. We can't put it off any longer... and the government seems to realize this.

Quanta should see even better returns going forward than it has before.

This isn't a one-time energy-infrastructure fix...

More folks are buying EVs... companies keep putting up data centers... and we're using more power by the day. Old power lines won't cut it anymore.

On Tuesday, we explained that investors are completely missing the opportunity in Fluor (FLR) – a C&E leader that's benefiting from infrastructure construction trends.

Folks seem to sort of get what's happening with Quanta. They just aren't pricing in its full potential.

As Quanta keeps breaking revenue records, shares can easily keep rising.

Regards,

Joel Litman

March 14, 2024