Eli Lilly (LLY) is going all in on weight-loss drugs...

Eli Lilly (LLY) is going all in on weight-loss drugs...

The pharmaceutical giant recently announced a $27 billion investment to build four new manufacturing plants in the U.S.

These plants would produce active pharmaceutical ingredients and sterile injectables, including Eli Lilly's blockbuster GLP-1 drug Mounjaro.

It would be one of the largest domestic expansions in the industry's history... And manufacturing would go live within five years.

This move tops the $23 billion Eli Lilly has already spent on U.S. operations in the past five years. Altogether, the company is on track to double its capital base by 2030.

At first glance, this level of spending might seem risky. But a closer look at the numbers tells a different story...

Today, we'll use Uniform Accounting principles to explain why Eli Lilly's aggressive spending isn't a red flag. In fact, it's preparing the company, and investors, for a great opportunity.

GLP-1 drug demand has skyrocketed in the past few years...

As we discussed in January, drugs like Mounjaro and Ozempic have become household names. Initially developed for diabetes, they're now prescribed for weight loss, metabolic health, and even cardiovascular support.

Analysts expect the GLP-1 market to grow by about $100 billion in the next decade. And Eli Lilly's response has been simple... Build as fast as possible to stay ahead of rising demand.

If the $27 billion initiative goes as planned, it would nearly double Eli Lilly's existing property, plant, and equipment value of $29 billion. It would also double its manufacturing investment.

For most companies, that magnitude of scaling can drag down profitability. But Eli Lilly isn't most companies... and GLP-1 drugs aren't an ordinary product.

Despite the company's stellar track record, the market still doubts Eli Lilly's ability to generate big returns...

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

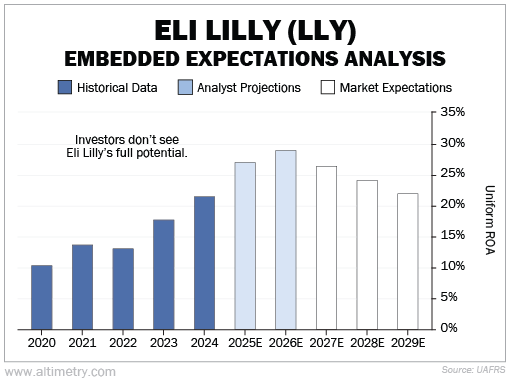

Eli Lilly's Uniform return on assets ("ROA") jumped from around 14% in 2021 (before GLP-1 drugs really entered the scene) to 21% in 2024. That's an exceptional rise in profitability for a mega-cap company.

And analysts are projecting its Uniform ROA to climb even higher, to 29% by 2026.

Despite the company's plans to double its asset base over the next five years (that's 15% growth per year), the market is only pricing in modest improvement. Take a look...

In other words, investors still doubt whether Eli Lilly can maintain, let alone boost, growing returns as it scales.

Given the rapidly expanding weight-loss drug market, investors should be more optimistic...

Demand for GLP-1 drugs is surging, and we expect it to keep climbing. This is putting firms like Eli Lilly in a strong position.

However, the company isn't just betting on GLP-1s... It's building the infrastructure to produce a wide range of pharmaceuticals.

Still, despite its massive investment, the market doesn't expect significant growth. That disconnect signals opportunity...

If product demand continues at the current rate, or anything close to it, Eli Lilly's earnings power could obliterate market expectations... And investors could then take advantage of the cheap stock.

Regards,

Joel Litman

April 2, 2025