American Airlines (AAL) didn't care about the competition...

American Airlines (AAL) didn't care about the competition...

Or at least, Vasu Raja didn't seem to.

Raja was American's commercial head from 2022 until this past May... when he was fired after two decades with the company.

American drastically changed its sales approach under Raja's leadership. He pushed it to attract customers through its own sales portals, rather than third-party websites.

The company pulled nearly 40% of its fares from third-party travel systems... most of which were its cheapest tickets.

In theory, the strategy gave American more control of its customer pipeline. In reality, customers – and corporate customers in particular – ended up paying way more for American flights.

Unsurprisingly, they weren't happy. This change undid a lot of goodwill American had built over the years.

And rather than reluctantly accepting it... these folks took their business to other air carriers.

As we'll cover today, American's stock has fallen on hard times... and it might look like a value play on the surface. However, it's not necessarily time to jump in yet.

Even with summer travel gearing up, American has a bleak outlook on all fronts...

Ticket prices soared in recent years, at least partly due to Raja's strategy. That brought down corporate demand... which meant a hit to revenue.

The company now forecasts a full-year revenue slide of 5% to 6% year over year, way worse than its previous expectations for a roughly 2% decline.

To make matters worse, American is dealing with disgruntled employees. Its flight attendant union is preparing to strike amid failing negotiations... which could lead to flight delays.

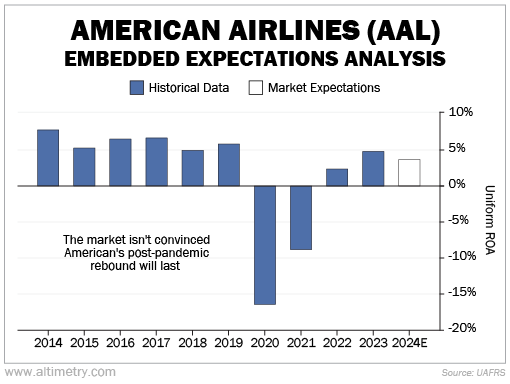

While 2023 was its best year since the pandemic, Uniform return on assets ("ROA") only reached 5%. That's less than half the 12% corporate average.

Shareholders are getting scared. We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from future cash flows.

We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

American saw a slight post-pandemic recovery. But in 2024, investors expect Uniform ROA to decrease... falling slightly below its 5% breakeven level.

Take a look...

Now that Raja is out, American is backpedaling on its aggressive pricing strategy. But the market isn't interested.

Shares are down about 17% year to date... almost back to a one-year low.

Investors don't think American has enough going for it to keep up the rebound...

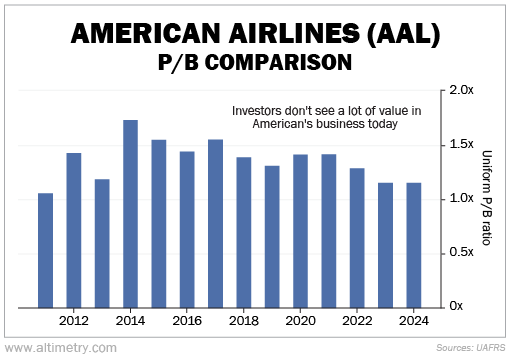

That's particularly true when you look at the Uniform price-to-book (P/B) ratio.

The P/B ratio compares a company's total value with the value of the assets on its balance sheet (or "book"). The higher the P/B ratio, the more investors are willing to pay for its assets.

Said another way, it measures how valuable investors think American's assets are.

A company normally trades below a Uniform P/B ratio of 1 when the market is worried about bankruptcy risk.

And while American is sitting above a 1 today... the recent sell-off has taken its toll. The company's P/B ratio is at the lower end of valuations in the past decade-plus.

Check it out...

As you can see, American isn't exactly in "bankruptcy cheap" territory. That said, by this measure, valuations haven't been this low since 2011.

American is unlikely to fall much further... but there's no guarantee this stock is due for a rebound.

As we mentioned, it lost a lot of goodwill as customers realized they were being forced into higher-priced ticket options.

This stock could be doomed to near-book valuations until American fixes the mess that Raja started.

Regards,

Joel Litman

June 26, 2024