Financial-services giant Goldman Sachs (GS) is preparing for the AI takeover...

Financial-services giant Goldman Sachs (GS) is preparing for the AI takeover...

It initially pinned down the capital-intensive businesses that could outperform as more vulnerable software firms lag behind.

These were Goldman's "HALO" trades – companies with "heavy assets and low obsolescence."

But it isn't writing software companies off entirely. Goldman is just shifting its investment strategy… The company is now "long" the capital-intensive (AI-proof) stocks and "short" the capital-light (AI-vulnerable) stocks.

Essentially, it's buying undervalued securities and short selling overvalued securities.

Between February 13, 2025 and February 13, 2026, Goldman's pair trade gained more than 60%. The software sector as a whole fell about 12% over the same period.

That tells us the market is starting to favor software businesses with real staying power over the ones AI can easily replace.

Today, we'll look at the major names on both sides of Goldman's software pair trade and how investors could potentially profit from a key imbalance in the market.

On the long side, Goldman is leaning into businesses that build, run, and/or protect AI infrastructure...

These include Microsoft (MSFT) – one of the biggest platforms for developing and distributing AI technology – and Palo Alto Networks (PANW), which provides network firewall technology.

Goldman also highlighted names tied to cloud infrastructure and data plumbing, like Cloudflare (NET) and Oracle (ORCL), respectively.

Security is becoming particularly important as AI expands globally and more sensitive data enters the pipeline. That's where companies like PANW come into play.

In this "long" basket, Goldman is focusing on software companies that are likely to become more valuable as AI adoption takes off.

Goldman's 'short' basket tells the other half of the story...

It includes software companies that are more vulnerable to AI, like language-learning app Duolingo (DUOL), e-signature business DocuSign (DOCU), and productivity tool Monday (MNDY).

Customer relationship management giant Salesforce (CRM) and business process outsourcing leader Accenture (ACN) are also part of the "short" basket.

Their digital tools are becoming easier and easier for AI to imitate. AI language translation, for example, is now almost as good as human translation.

But there's no reason you'll have to use Duolingo to translate or learn languages. Similarly, you won't have to use DocuSign to digitally sign all your documents.

There are a lot of popular options out there. And AI will only ramp up competition across all these industries.

Yet, investors don't fully understand what's going on in the market...

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

The AI-proof long basket has been very profitable... Its Uniform return on assets ("ROA") has stayed above 30% every year since 2021.

After the recent software sell-off, expectations dipped. Investors expect this basket's Uniform ROA to fall to 26% through the next few years. Take a look...

Companies like Microsoft and Oracle are better equipped to hold up against the AI disruption. But investors have marked them down, along with the rest of the tech sector.

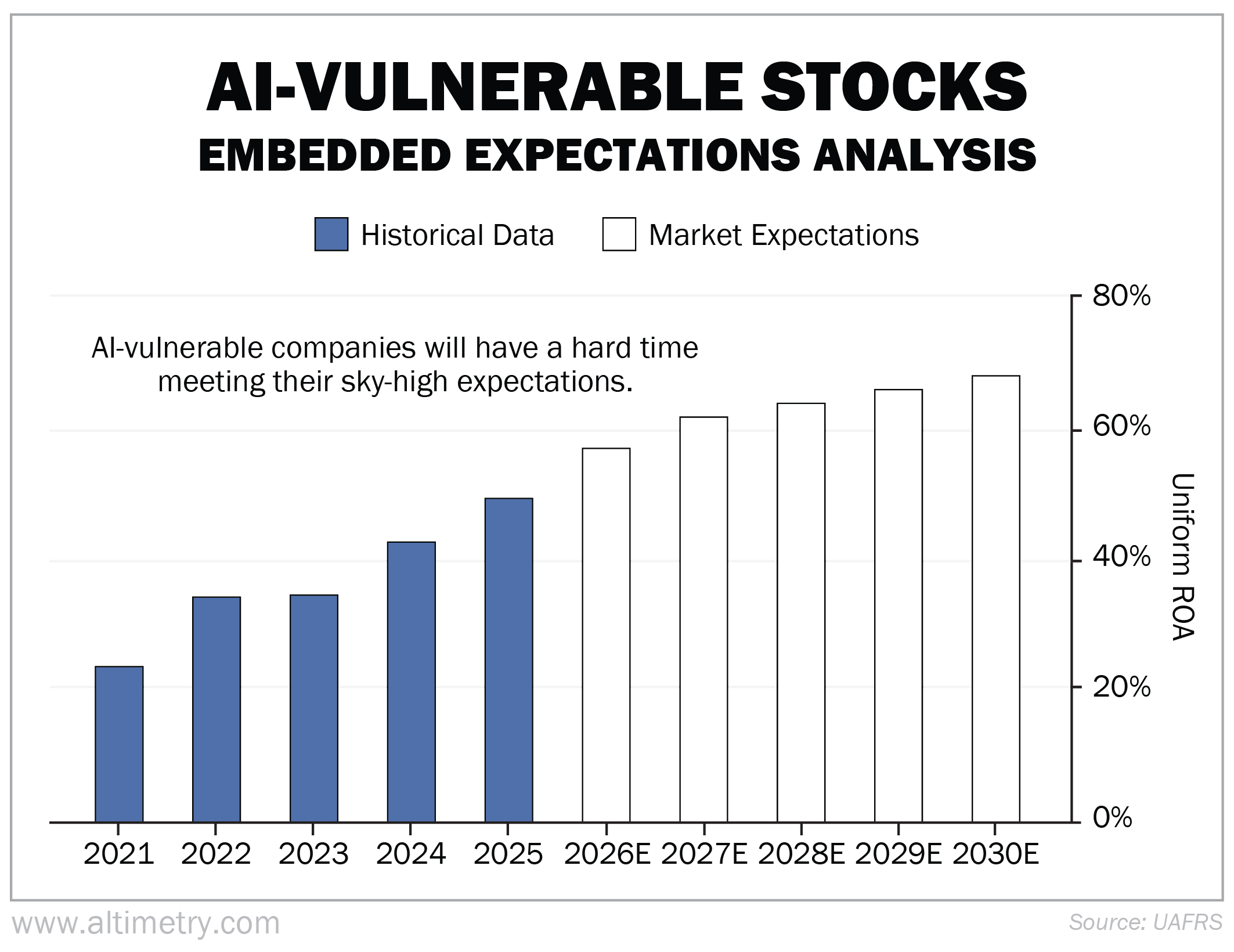

On the other hand, the short basket has produced a surprisingly strong Uniform ROA... It jumped from 24% in 2021 to 49% last year.

These companies shot up because their products were novel, cheap to maintain, and easy to sell. Current valuations suggest they'll need to reach a Uniform ROA of about 68% (on average) to justify today's prices. Take a look...

These AI-vulnerable stocks are still too expensive. That's a steep hurdle for businesses whose products are becoming easier to duplicate.

Goldman's pair trade is capitalizing on the imbalance between these two software baskets.

The longs have stronger moats and lower expectations. The shorts have shakier moats and much higher expectations...

Investors need to ask themselves one question...

Which software businesses are durable enough to survive as AI gets cheaper, faster, and easier to use?

The answer is, the companies that offer diverse app functionalities... leverage proprietary data... and prioritize security.

These are the features AI will have trouble competing with over time.

So far, investors haven't figured this out. That's why you've got expensive AI-vulnerable stocks and cheap AI-proof stocks.

If you understand Goldman's pair trade, you can position yourself to make good money once the market corrects this inequality.

Regards,

Joel Litman

March 26, 2026