Editor's note: Every Monday for the next few weeks, we'll spend some time digging into the similarities between the U.S. economy after World War II and today. Be sure to check back each week to keep up with our coverage of the timeline.

Investors are starting to believe the Fed...

As we discussed last week, the central bank's latest measures are proving that it's serious about controlling inflation.

So instead, the market is turning to its next scary buzzword – recession.

As markets tanked in mid-June and Fed Chairman Jerome Powell made it known that a 0.75% interest-rate hike was on the table, Google Trends searches for "Recession" skyrocketed.

They spiked to 30 times higher than they were at the beginning of the year... and 5 times higher than they were just two weeks earlier in late May.

The logic goes like this... If the Fed is really going to tamp down inflation, it's going to have to force a recession right now. And we don't just mean the false recession that we may currently be seeing, either.

But history shows that things might not play out the way Wall Street expects...

After the Fed got serious about fighting inflation in 1947, the market didn't continue to tank. It traded basically sideways for a year and a half after the Fed started raising rates.

And while inflation came down, the economy didn't come crashing down with it...

Nominal U.S. gross domestic product ("GDP") growth remained strong, up 10% in both 1947 and 1948. Corporate defaults remained low, too. Unemployment rates were largely steady at 3.9% in 1946 and 4% at the end of 1948.

Put simply, the economy kept humming along.

As we explained two weeks ago, inflation had occurred because of booming demand. The Fed's actions spread out that demand and reduced inflation, rather than smothering economic spending.

The demand was still there, thanks to all that pent-up wartime saving. So growth remained strong.

Remember, as we've said many times before, rising rates aren't bad for the economy.

In reality, rate hikes mean the economy is booming... and banks and regulators are trying to temper that growth. It's when interest rates become too high that the economy gets into trouble.

That's the environment we're faced with today...

Strong post-pandemic demand in the U.S. and around the world... strained supply chains... and geopolitical tensions have all come together to create this inflation.

As we mentioned two weeks ago, the injection of $4 trillion of personal savings into the U.S. economy has helped contribute to this boom.

And that booming demand is why nominal GDP growth was 6% last quarter. That's why research firm The Conference Board forecasts nominal GDP growth of about 7% in the second quarter, based on real GDP and inflation expectations.

The strong economy is why unemployment still sits at 3.6%. It's why corporate loan charge-offs are at historically low levels. And it's why consumer loan delinquency rates are low as well.

The Fed's rate hikes aren't going to force a strong economy into a real recession immediately. The economy is doing too well for that... just like it was in 1947 and 1948.

To understand when high interest rates might bite, we can look deeper into the credit markets...

There are two big factors that turn rising interest rates into rates that are too high for the economy to bear. In short, it's all about debt maturities and profitability.

If borrowers don't have any debt coming due that they need to reprice, then it won't cause a recession – even as interest rates rise. Sure, it will cause slower growth because people will borrow less to finance investments... That doesn't cause a recession, though.

Credit destruction is what causes a recession.

When a borrower can't service its debt, it causes a chain reaction. People will go to the bank to see about refinancing debt, and the bank won't be able to cover the higher interest payments. So it will have to default.

After defaulting, the bank won't spend as much. Other borrowers' profitability will decline, and then their income won't cover their interest expenses. Ultimately, they'll default as well.

Credit destruction feeds on itself until it washes out.

We can tell that didn't happen in 1947 and 1948 because of the lack of corporate defaults. And it isn't happening now because our economy is so strong.

But if the Fed keeps raising rates, we'll need to keep an eye out for big debt-maturity headwalls. That's a fancy way of saying that we're looking for times when lots of debt come due at once.

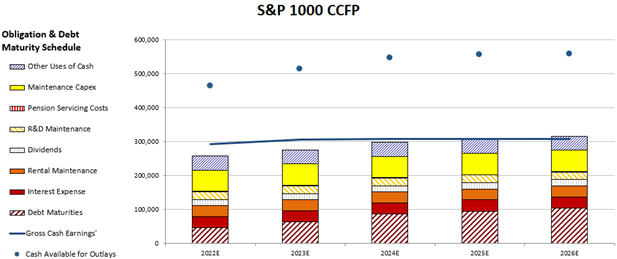

Right now, our Credit Cash Flow Prime ("CCFP") analysis shows that the nearest U.S. corporate debt-maturity headwalls might be in 2025... or 2024 at the earliest. This means we have time to tackle inflation before companies have to make tough decisions about their debt that could create a vicious cycle of defaults.

Until 2024, cash flows alone more than exceed all of the average company's obligations, and debt maturities are modest. This is thanks to the wave of refinancing that happened in 2020 and 2021, when interest rates were extraordinarily low.

If the Fed can effectively moderate inflation before those headwalls start to impact the economy, there's the chance that it could thread the needle.

Next week, we'll explain what happened the last time the Fed faced a setup like this. Be sure to check back in for the latest installment in this series.

Investors are starting to believe the Fed...

Investors are starting to believe the Fed...